Futures Data Processing Walkthrough#

This notebook demonstrates the data processing pipeline for equity index futures data, which is a critical component of our equity spot-futures arbitrage analysis project.

Project Context: Equity Spot-Futures Arbitrage#

Our project analyzes arbitrage opportunities between equity spot and futures markets, focusing on three major indices:

S&P 500 (SPX with ES futures)

Nasdaq 100 (NDX with NQ futures)

Dow Jones Industrial Average (INDU with DM futures)

To calculate implied forward rates for arbitrage analysis, we need properly processed futures data with accurate settlement dates and time-to-maturity calculations.

import pandas as pd

import numpy as np

from datetime import datetime, timedelta

import calendar

import logging

import sys

import os

import matplotlib.pyplot as plt

import seaborn as sns

from pathlib import Path

%matplotlib inline

sns.set_style('whitegrid')

# Add the src directory to the path to import our settings

sys.path.insert(1, "./src")

try:

from settings import config

print("Successfully imported config from settings module")

except ImportError:

print("Failed to import config. Make sure your working directory is set correctly.")

def config(key):

config_dict = {

"DATA_DIR": Path("./_data"),

"TEMP_DIR": Path("./_data/temp"),

"INPUT_DIR": Path("./_data/input"),

"PROCESSED_DIR": Path("./_data/processed"),

"MANUAL_DATA_DIR": Path("./data_manual"),

"OUTPUT_DIR":Path("./_output"),

}

return config_dict.get(key, Path("./data"))

Successfully imported config from settings module

Load Libraries#

# Load configuration paths

DATA_DIR = config("DATA_DIR")

TEMP_DIR = config("TEMP_DIR")

INPUT_DIR = config("INPUT_DIR")

PROCESSED_DIR = config("PROCESSED_DIR")

DATA_MANUAL = config("MANUAL_DATA_DIR")

OUTPUT_DIR = config("OUTPUT_DIR")

# Create directories if they don't exist

for dir_path in [DATA_DIR, TEMP_DIR, INPUT_DIR, PROCESSED_DIR, DATA_MANUAL]:

os.makedirs(dir_path, exist_ok=True)

# Set up logging

log_file = TEMP_DIR / 'futures_processing_notebook.log'

logging.basicConfig(

level=logging.INFO,

format='%(asctime)s - %(levelname)s - %(message)s',

handlers=[

logging.FileHandler(log_file),

logging.StreamHandler(sys.stdout)

]

)

logger = logging.getLogger(__name__)

logger.info("Logging configured successfully")

logger.info(f"Log file will be saved to: {log_file}")

2025-03-11 04:10:26,143 - INFO - Logging configured successfully

2025-03-11 04:10:26,144 - INFO - Log file will be saved to: C:\Users\Andik\OneDrive\Desktop\Chicago\Full_stack_QF\Equity_Spot_futures_arb\_output\temp\futures_processing_notebook.log

Define Utility Functions#

We need several utility functions to properly process futures contract data:

def get_third_friday(year, month):

"""

Calculate the third Friday of a given month and year.

Args:

year (int): Year

month (int): Month (1-12)

Returns:

datetime: Date object for the third Friday

"""

# Use calendar.monthcalendar: each week is a list of ints (0 if day not in month)

month_cal = calendar.monthcalendar(year, month)

# The first week that has a Friday (weekday index 4)

fridays = [week[calendar.FRIDAY] for week in month_cal if week[calendar.FRIDAY] != 0]

if len(fridays) < 3:

raise ValueError(f"Not enough Fridays in {year}-{month}")

return datetime(year, month, fridays[2]) # third Friday

def parse_contract_month_year(contract_str):

"""

Parse Bloomberg's contract month/year string (e.g., 'DEC 10') into

a month number and a full year.

Args:

contract_str (str): Contract month/year string

Returns:

tuple: (month_num, year_full) or (None, None) if invalid.

"""

if pd.isna(contract_str) or contract_str.strip() == '':

return None, None

parts = contract_str.split()

if len(parts) != 2:

logger.warning(f"Unexpected contract format: {contract_str}")

return None, None

month_abbr, year_abbr = parts

allowed = {"MAR": 3, "JUN": 6, "SEP": 9, "DEC": 12}

if month_abbr.upper() not in allowed:

raise ValueError(f"Contract month {month_abbr} not in allowed set {list(allowed.keys())}")

month_num = allowed[month_abbr.upper()]

try:

yr = int(year_abbr)

year_full = 2000 + yr if yr < 50 else 1900 + yr

except ValueError:

logger.warning(f"Could not parse year: {year_abbr}")

return None, None

return month_num, year_full

# Test our utility functions with a couple of examples

print(f"Third Friday of March 2023: {get_third_friday(2023, 3)}")

print(f"Parsing 'DEC 22': {parse_contract_month_year('DEC 22')}")

print(f"Parsing 'MAR 23': {parse_contract_month_year('MAR 23')}")

Third Friday of March 2023: 2023-03-17 00:00:00

Parsing 'DEC 22': (12, 2022)

Parsing 'MAR 23': (3, 2023)

Load Bloomberg Data#

Let’s load the Bloomberg futures data from the Parquet file:

try:

INPUT_FILE = INPUT_DIR / "bloomberg_historical_data.parquet"

if not os.path.exists(INPUT_FILE):

logger.warning("Primary input file not found, switching to cached data")

INPUT_FILE = DATA_MANUAL / "bloomberg_historical_data.parquet"

raw_data = pd.read_parquet(INPUT_FILE)

logger.info(f"Successfully loaded data from {INPUT_FILE}")

# Convert index to DatetimeIndex if it's not already

if not isinstance(raw_data.index, pd.DatetimeIndex):

raw_data.index = pd.to_datetime(raw_data.index)

logger.info("Converted index to DatetimeIndex")

# Display the column structure (MultiIndex)

logger.info(f"Column levels: {raw_data.columns.names}")

print("\nSample of MultiIndex columns:")

for i, col in enumerate(raw_data.columns[:10]):

print(f" {col}")

print(f" ...and {len(raw_data.columns)-10} more columns")

# Display basic info about the dataset

print(f"\nDataset shape: {raw_data.shape}")

print(f"Date range: {raw_data.index.min()} to {raw_data.index.max()}")

except Exception as e:

logger.error(f"Error loading data: {e}")

raise

2025-03-11 04:10:26,229 - WARNING - Primary input file not found, switching to cached data

2025-03-11 04:10:26,437 - INFO - Successfully loaded data from C:\Users\Andik\OneDrive\Desktop\Chicago\Full_stack_QF\Equity_Spot_futures_arb\data_manual\bloomberg_historical_data.parquet

2025-03-11 04:10:26,440 - INFO - Column levels: [None, None]

Sample of MultiIndex columns:

('SPX Index', 'PX_LAST')

('SPX Index', 'IDX_EST_DVD_YLD')

('SPX Index', 'INDX_GROSS_DAILY_DIV')

('NDX Index', 'PX_LAST')

('NDX Index', 'IDX_EST_DVD_YLD')

('NDX Index', 'INDX_GROSS_DAILY_DIV')

('INDU Index', 'PX_LAST')

('INDU Index', 'IDX_EST_DVD_YLD')

('INDU Index', 'INDX_GROSS_DAILY_DIV')

('ES1 Index', 'PX_LAST')

...and 52 more columns

Dataset shape: (3913, 62)

Date range: 2010-01-01 00:00:00 to 2024-12-31 00:00:00

Define Index Futures Mapping#

Let’s define the mapping between equity indices and their futures contracts:

indices = {

'SPX': ['ES1', 'ES2', 'ES3', 'ES4'], # S&P 500 futures

'NDX': ['NQ1', 'NQ2', 'NQ3', 'NQ4'], # Nasdaq 100 futures

'INDU': ['DM1', 'DM2', 'DM3', 'DM4'] # Dow Jones futures

}

print("Equity indices and their futures contracts:")

for index, futures in indices.items():

print(f" {index}: {', '.join(futures)}")

Equity indices and their futures contracts:

SPX: ES1, ES2, ES3, ES4

NDX: NQ1, NQ2, NQ3, NQ4

INDU: DM1, DM2, DM3, DM4

Process Futures Data#

Now, let’s implement the function that processes futures data for a single index:

def process_index_futures(data, futures_codes):

"""

Process futures data for one index.

Args:

data (pd.DataFrame): Multi-index DataFrame with Bloomberg data (indexed by Date)

futures_codes (list): List of futures codes (e.g., ['ES1', 'ES2', ...])

Returns:

dict: Dictionary of processed DataFrames, one for each futures code.

Each DataFrame contains:

- Date

- Futures_Price (from PX_LAST)

- Volume, OpenInterest (if available)

- ContractSpec (raw CURRENT_CONTRACT_MONTH_YR)

- SettlementDate (actual settlement, 3rd Friday)

- TTM (time-to-maturity in days)

"""

result_dfs = {}

for code in futures_codes:

logger.info(f"Processing futures data for {code} Index")

try:

# Extract columns for this contract

price_series = data.loc[:, (f'{code} Index', 'PX_LAST')]

volume_series = data.loc[:, (f'{code} Index', 'PX_VOLUME')]

oi_series = data.loc[:, (f'{code} Index', 'OPEN_INT')]

contract_series = data.loc[:, (f'{code} Index', 'CURRENT_CONTRACT_MONTH_YR')]

# Create a DataFrame for this contract; index is Date (from raw data)

df_contract = pd.DataFrame({

'Date': data.index,

'Futures_Price': price_series,

'Volume': volume_series,

'OpenInterest': oi_series,

'ContractSpec': contract_series

})

df_contract = df_contract.reset_index(drop=True)

# Parse contract specification and compute settlement date

settlement_dates = []

for cs in df_contract['ContractSpec']:

month_num, year_full = parse_contract_month_year(cs)

if month_num is None or year_full is None:

settlement_dates.append(None)

else:

settlement_dates.append(get_third_friday(year_full, month_num))

df_contract['SettlementDate'] = pd.to_datetime(settlement_dates)

# Compute TTM in days: SettlementDate - Date

df_contract['Date'] = pd.to_datetime(df_contract['Date'])

df_contract['TTM'] = (df_contract['SettlementDate'] - df_contract['Date']).dt.days

# Drop rows with missing TTM (if settlement date couldn't be computed)

df_contract = df_contract.dropna(subset=['TTM'])

result_dfs[code] = df_contract

logger.info(f"Processed {code}: {len(df_contract)} rows")

except Exception as e:

logger.error(f"Error processing {code}: {e}")

continue

return result_dfs

Process All Indices#

Let’s apply our processing function to all indices:

all_futures = {}

for index_code, futures_codes in indices.items():

logger.info(f"Processing futures for index {index_code}")

processed = process_index_futures(raw_data, futures_codes)

all_futures[index_code] = processed

# Display a sample of the processed data for each index

print(f"\nProcessed Futures for {index_code}:")

for code, df in processed.items():

print(f" {code} - Shape: {df.shape}")

display(df.head(3))

2025-03-11 04:10:26,567 - INFO - Processing futures for index SPX

2025-03-11 04:10:26,571 - INFO - Processing futures data for ES1 Index

2025-03-11 04:10:26,729 - INFO - Processed ES1: 3781 rows

2025-03-11 04:10:26,731 - INFO - Processing futures data for ES2 Index

2025-03-11 04:10:26,871 - INFO - Processed ES2: 3781 rows

2025-03-11 04:10:26,876 - INFO - Processing futures data for ES3 Index

2025-03-11 04:10:27,017 - INFO - Processed ES3: 3781 rows

2025-03-11 04:10:27,021 - INFO - Processing futures data for ES4 Index

2025-03-11 04:10:27,158 - INFO - Processed ES4: 3781 rows

Processed Futures for SPX:

ES1 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1128.75 | 1282633.0 | 2440458.0 | MAR 10 | 2010-03-19 | 74.0 |

| 2 | 2010-01-05 | 1132.25 | 1368386.0 | 2402850.0 | MAR 10 | 2010-03-19 | 73.0 |

| 3 | 2010-01-06 | 1133.00 | 1252015.0 | 2396493.0 | MAR 10 | 2010-03-19 | 72.0 |

ES2 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1124.0 | 1641.0 | 3354.0 | JUN 10 | 2010-06-18 | 165.0 |

| 2 | 2010-01-05 | 1127.5 | 686.0 | 3432.0 | JUN 10 | 2010-06-18 | 164.0 |

| 3 | 2010-01-06 | 1128.0 | 1163.0 | 3713.0 | JUN 10 | 2010-06-18 | 163.0 |

ES3 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1119.5 | 100.0 | 439.0 | SEP 10 | 2010-09-17 | 256.0 |

| 2 | 2010-01-05 | 1123.0 | 300.0 | 539.0 | SEP 10 | 2010-09-17 | 255.0 |

| 3 | 2010-01-06 | 1123.5 | 601.0 | 1140.0 | SEP 10 | 2010-09-17 | 254.0 |

ES4 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1116.5 | NaN | 6.0 | DEC 10 | 2010-12-17 | 347.0 |

| 2 | 2010-01-05 | 1120.0 | 4.0 | 8.0 | DEC 10 | 2010-12-17 | 346.0 |

| 3 | 2010-01-06 | 1120.5 | NaN | 8.0 | DEC 10 | 2010-12-17 | 345.0 |

2025-03-11 04:10:27,244 - INFO - Processing futures for index NDX

2025-03-11 04:10:27,251 - INFO - Processing futures data for NQ1 Index

2025-03-11 04:10:27,394 - INFO - Processed NQ1: 3781 rows

2025-03-11 04:10:27,398 - INFO - Processing futures data for NQ2 Index

2025-03-11 04:10:27,554 - INFO - Processed NQ2: 3781 rows

2025-03-11 04:10:27,560 - INFO - Processing futures data for NQ3 Index

2025-03-11 04:10:27,714 - INFO - Processed NQ3: 3781 rows

2025-03-11 04:10:27,718 - INFO - Processing futures data for NQ4 Index

2025-03-11 04:10:27,869 - INFO - Processed NQ4: 3781 rows

Processed Futures for NDX:

NQ1 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1886.75 | 204140.0 | 314877.0 | MAR 10 | 2010-03-19 | 74.0 |

| 2 | 2010-01-05 | 1885.25 | 207245.0 | 309080.0 | MAR 10 | 2010-03-19 | 73.0 |

| 3 | 2010-01-06 | 1878.50 | 259627.0 | 310532.0 | MAR 10 | 2010-03-19 | 72.0 |

NQ2 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1884.75 | 33.0 | 671.0 | JUN 10 | 2010-06-18 | 165.0 |

| 2 | 2010-01-05 | 1883.00 | 74.0 | 651.0 | JUN 10 | 2010-06-18 | 164.0 |

| 3 | 2010-01-06 | 1876.50 | 33.0 | 665.0 | JUN 10 | 2010-06-18 | 163.0 |

NQ3 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1883.75 | NaN | NaN | SEP 10 | 2010-09-17 | 256.0 |

| 2 | 2010-01-05 | 1882.00 | NaN | NaN | SEP 10 | 2010-09-17 | 255.0 |

| 3 | 2010-01-06 | 1875.50 | NaN | NaN | SEP 10 | 2010-09-17 | 254.0 |

NQ4 - Shape: (3781, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 1882.75 | NaN | 2.0 | DEC 10 | 2010-12-17 | 347.0 |

| 2 | 2010-01-05 | 1881.00 | NaN | 2.0 | DEC 10 | 2010-12-17 | 346.0 |

| 3 | 2010-01-06 | 1874.50 | NaN | 2.0 | DEC 10 | 2010-12-17 | 345.0 |

2025-03-11 04:10:27,959 - INFO - Processing futures for index INDU

2025-03-11 04:10:27,961 - INFO - Processing futures data for DM1 Index

2025-03-11 04:10:28,110 - INFO - Processed DM1: 3780 rows

2025-03-11 04:10:28,111 - INFO - Processing futures data for DM2 Index

2025-03-11 04:10:28,252 - INFO - Processed DM2: 3780 rows

2025-03-11 04:10:28,255 - INFO - Processing futures data for DM3 Index

2025-03-11 04:10:28,430 - INFO - Processed DM3: 3780 rows

2025-03-11 04:10:28,435 - INFO - Processing futures data for DM4 Index

2025-03-11 04:10:28,591 - INFO - Processed DM4: 3780 rows

Processed Futures for INDU:

DM1 - Shape: (3780, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 10519.0 | 93770.0 | 69420.0 | MAR 10 | 2010-03-19 | 74.0 |

| 2 | 2010-01-05 | 10515.0 | 93287.0 | 65749.0 | MAR 10 | 2010-03-19 | 73.0 |

| 3 | 2010-01-06 | 10516.0 | 97172.0 | 63888.0 | MAR 10 | 2010-03-19 | 72.0 |

DM2 - Shape: (3780, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 10459.0 | 100.0 | 175.0 | JUN 10 | 2010-06-18 | 165.0 |

| 2 | 2010-01-05 | 10455.0 | 26.0 | 173.0 | JUN 10 | 2010-06-18 | 164.0 |

| 3 | 2010-01-06 | 10455.0 | 157.0 | 193.0 | JUN 10 | 2010-06-18 | 163.0 |

DM3 - Shape: (3780, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 10404.0 | NaN | 1.0 | SEP 10 | 2010-09-17 | 256.0 |

| 2 | 2010-01-05 | 10400.0 | NaN | 1.0 | SEP 10 | 2010-09-17 | 255.0 |

| 3 | 2010-01-06 | 10400.0 | NaN | 2.0 | SEP 10 | 2010-09-17 | 254.0 |

DM4 - Shape: (3780, 7)

| Date | Futures_Price | Volume | OpenInterest | ContractSpec | SettlementDate | TTM | |

|---|---|---|---|---|---|---|---|

| 1 | 2010-01-04 | 10354.0 | NaN | NaN | DEC 10 | 2010-12-17 | 347.0 |

| 2 | 2010-01-05 | 10350.0 | NaN | NaN | DEC 10 | 2010-12-17 | 346.0 |

| 3 | 2010-01-06 | 10351.0 | NaN | NaN | DEC 10 | 2010-12-17 | 345.0 |

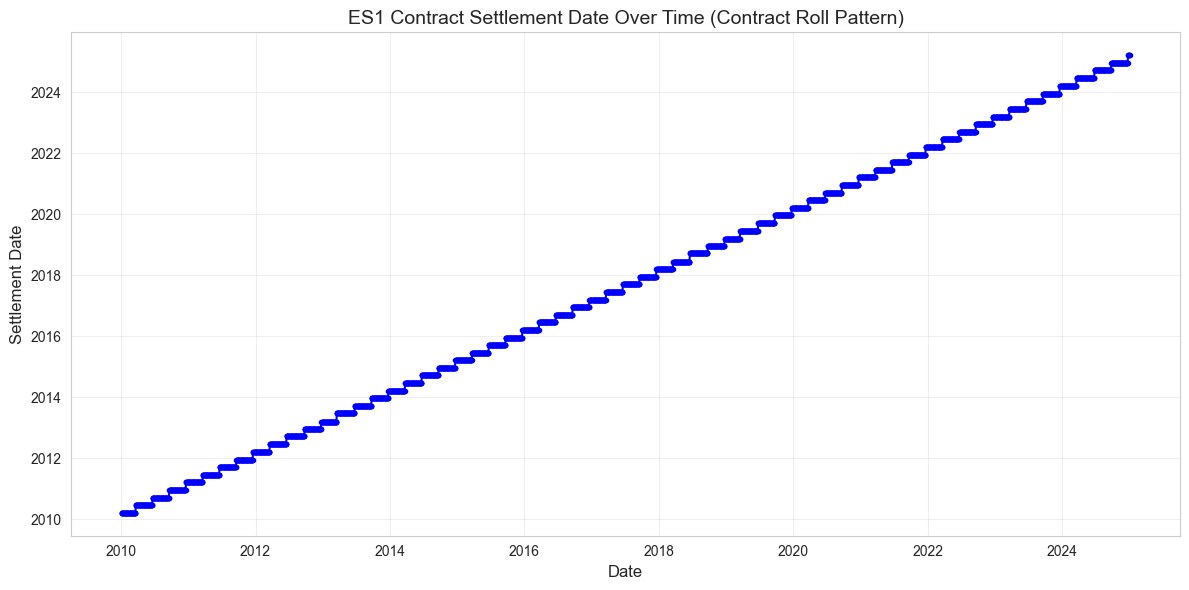

Analyze Contract Roll Patterns#

Let’s visualize how contracts roll over time for one of the indices:

# Choose SPX ES1 (front-month) contract for visualization

es1_df = all_futures['SPX']['ES1']

# Plot settlement date changes over time to visualize contract rolls

plt.figure(figsize=(12, 6))

plt.plot(es1_df['Date'], es1_df['SettlementDate'], 'b.-')

plt.title('ES1 Contract Settlement Date Over Time (Contract Roll Pattern)', fontsize=14)

plt.xlabel('Date', fontsize=12)

plt.ylabel('Settlement Date', fontsize=12)

plt.grid(True, alpha=0.3)

plt.tight_layout()

# Save the visualization

plt.savefig(OUTPUT_DIR / 'es1_contract_roll_pattern.png', dpi=300)

plt.show()

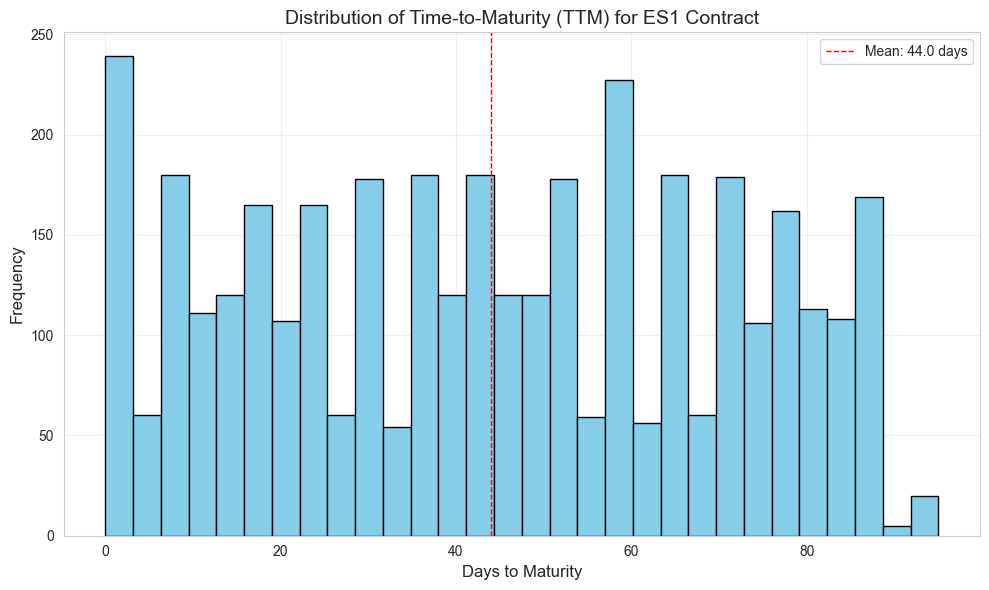

# Analyze TTM distribution for ES1

plt.figure(figsize=(10, 6))

plt.hist(es1_df['TTM'], bins=30, color='skyblue', edgecolor='black')

plt.axvline(es1_df['TTM'].mean(), color='red', linestyle='dashed', linewidth=1, label=f'Mean: {es1_df["TTM"].mean():.1f} days')

plt.title('Distribution of Time-to-Maturity (TTM) for ES1 Contract', fontsize=14)

plt.xlabel('Days to Maturity', fontsize=12)

plt.ylabel('Frequency', fontsize=12)

plt.grid(True, alpha=0.3)

plt.legend()

plt.tight_layout()

# Save the visualization

plt.savefig(OUTPUT_DIR / 'es1_ttm_distribution.png', dpi=300)

plt.show()

Create Calendar Spreads#

Now let’s implement the function to merge the Term 1 (nearest) and Term 2 (next nearest) contracts to create calendar spreads:

def merge_calendar_spreads(all_futures):

"""

For each index, merge the processed data for the two nearest futures contracts (Term 1 and Term 2)

on the Date field, and then combine the calendar spreads for all indices.

Args:

all_futures (dict): Dictionary keyed by index code (e.g., 'SPX', 'NDX', 'INDU') where the value is

another dictionary mapping futures code to its processed DataFrame.

Returns:

pd.DataFrame: Combined calendar spread data for all indices.

"""

combined = []

# For each index, the first two codes are the two nearest contracts.

for index_code, fut_dict in all_futures.items():

# Identify term1 and term2 codes:

codes = list(fut_dict.keys())

if len(codes) < 2:

logger.warning(f"Not enough futures data for {index_code}")

continue

term1 = fut_dict[codes[0]].copy()

term2 = fut_dict[codes[1]].copy()

# Add a prefix so that we can merge and distinguish columns:

term1 = term1.add_prefix('Term1_')

term2 = term2.add_prefix('Term2_')

# Rename the Date columns back to 'Date' for merging

term1.rename(columns={'Term1_Date': 'Date'}, inplace=True)

term2.rename(columns={'Term2_Date': 'Date'}, inplace=True)

merged = pd.merge(term1, term2, on='Date', how='inner')

merged['Index'] = index_code

combined.append(merged)

if combined:

combined_df = pd.concat(combined, ignore_index=True)

return combined_df

else:

logger.warning("No valid calendar spread data to combine")

return None

Create and Analyze Calendar Spreads#

Let’s apply the function to create calendar spreads and analyze the results:

# Create calendar spreads

combined_spreads = merge_calendar_spreads(all_futures)

# Display a sample of the calendar spread data

print("Sample of Combined Calendar Spread Data:")

display(combined_spreads.head())

# Check key statistics for calendar spreads

print("\nCalendar Spread Statistics by Index:")

for index in combined_spreads['Index'].unique():

index_df = combined_spreads[combined_spreads['Index'] == index]

print(f"\n{index} Index:")

print(f" Number of observations: {len(index_df)}")

print(f" Average Term1 TTM: {index_df['Term1_TTM'].mean():.2f} days")

print(f" Average Term2 TTM: {index_df['Term2_TTM'].mean():.2f} days")

print(f" Average calendar spread (TTM2 - TTM1): {(index_df['Term2_TTM'] - index_df['Term1_TTM']).mean():.2f} days")

Sample of Combined Calendar Spread Data:

| Date | Term1_Futures_Price | Term1_Volume | Term1_OpenInterest | Term1_ContractSpec | Term1_SettlementDate | Term1_TTM | Term2_Futures_Price | Term2_Volume | Term2_OpenInterest | Term2_ContractSpec | Term2_SettlementDate | Term2_TTM | Index | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-04 | 1128.75 | 1282633.0 | 2440458.0 | MAR 10 | 2010-03-19 | 74.0 | 1124.00 | 1641.0 | 3354.0 | JUN 10 | 2010-06-18 | 165.0 | SPX |

| 1 | 2010-01-05 | 1132.25 | 1368386.0 | 2402850.0 | MAR 10 | 2010-03-19 | 73.0 | 1127.50 | 686.0 | 3432.0 | JUN 10 | 2010-06-18 | 164.0 | SPX |

| 2 | 2010-01-06 | 1133.00 | 1252015.0 | 2396493.0 | MAR 10 | 2010-03-19 | 72.0 | 1128.00 | 1163.0 | 3713.0 | JUN 10 | 2010-06-18 | 163.0 | SPX |

| 3 | 2010-01-07 | 1137.50 | 1553963.0 | 2406352.0 | MAR 10 | 2010-03-19 | 71.0 | 1132.50 | 1135.0 | 4154.0 | JUN 10 | 2010-06-18 | 162.0 | SPX |

| 4 | 2010-01-08 | 1141.50 | 1508175.0 | 2758348.0 | MAR 10 | 2010-03-19 | 70.0 | 1136.75 | 1080.0 | 17466.0 | JUN 10 | 2010-06-18 | 161.0 | SPX |

Calendar Spread Statistics by Index:

SPX Index:

Number of observations: 3781

Average Term1 TTM: 44.01 days

Average Term2 TTM: 135.33 days

Average calendar spread (TTM2 - TTM1): 91.32 days

NDX Index:

Number of observations: 3781

Average Term1 TTM: 44.01 days

Average Term2 TTM: 135.33 days

Average calendar spread (TTM2 - TTM1): 91.32 days

INDU Index:

Number of observations: 3780

Average Term1 TTM: 44.01 days

Average Term2 TTM: 135.32 days

Average calendar spread (TTM2 - TTM1): 91.32 days

It makes sense that the average calendar spread is over 3 months between contract 1 and contract 2

Data Quality Checks#

Let’s perform some data quality checks on our processed futures data:

def check_futures_data_quality(combined_spreads):

"""

Perform data quality checks on the processed futures data.

"""

print("Running data quality checks on futures data...")

tests_passed = 0

tests_failed = 0

# Test 1: Check that we have data for all three indices

try:

expected_indices = {'SPX', 'NDX', 'INDU'}

actual_indices = set(combined_spreads['Index'].unique())

assert expected_indices == actual_indices, f"Missing indices: {expected_indices - actual_indices}"

print(f"Test 1 Passed: All three indices are present")

tests_passed += 1

except AssertionError as e:

print(f"Test 1 Failed: {e}")

tests_failed += 1

# Test 2: Check that Term2_TTM > Term1_TTM for all rows

try:

assert all(combined_spreads['Term2_TTM'] > combined_spreads['Term1_TTM']), "Term2 TTM should always be greater than Term1 TTM"

print(f"Test 2 Passed: Term2 TTM is always greater than Term1 TTM")

tests_passed += 1

except AssertionError as e:

print(f"Test 2 Failed: {e}")

tests_failed += 1

# Test 3: Check that all TTM values are reasonable (positive and typically under 365 days)

try:

assert all(combined_spreads['Term1_TTM'] > 0), "Term1 TTM should be positive"

assert all(combined_spreads['Term2_TTM'] > 0), "Term2 TTM should be positive"

assert combined_spreads['Term1_TTM'].max() < 365, "Term1 TTM should typically be less than 365 days"

assert combined_spreads['Term2_TTM'].max() < 730, "Term2 TTM should typically be less than 730 days"

print(f"Test 3 Passed: TTM values are within reasonable ranges")

tests_passed += 1

except AssertionError as e:

print(f"Test 3 Failed: {e}")

tests_failed += 1

# Test 4: Check for missing values in critical columns

critical_columns = ['Term1_Futures_Price', 'Term2_Futures_Price', 'Term1_TTM', 'Term2_TTM']

try:

for col in critical_columns:

assert combined_spreads[col].isna().sum() == 0, f"Missing values in {col}"

print(f"Test 4 Passed: No missing values in critical columns")

tests_passed += 1

except AssertionError as e:

print(f"Test 4 Failed: {e}")

tests_failed += 1

# Test 5: Check that futures prices are positive

try:

assert all(combined_spreads['Term1_Futures_Price'] > 0), "Term1 futures prices should be positive"

assert all(combined_spreads['Term2_Futures_Price'] > 0), "Term2 futures prices should be positive"

print(f"Test 5 Passed: All futures prices are positive")

tests_passed += 1

except AssertionError as e:

print(f"Test 5 Failed: {e}")

tests_failed += 1

print(f"\nData quality checks complete: {tests_passed} passed, {tests_failed} failed")

return tests_passed, tests_failed

# Run the data quality checks

tests_passed, tests_failed = check_futures_data_quality(combined_spreads)

def check_futures_data_quality(combined_spreads):

"""

Perform data quality checks on the processed futures data.

"""

print("Running data quality checks on futures data...")

tests_passed = 0

tests_failed = 0

# Test 1: Check that we have data for all three indices

try:

expected_indices = {'SPX', 'NDX', 'INDU'}

actual_indices = set(combined_spreads['Index'].unique())

assert expected_indices == actual_indices, f"Missing indices: {expected_indices - actual_indices}"

print(f"Test 1 Passed: All three indices are present")

tests_passed += 1

except AssertionError as e:

print(f"Test 1 Failed: {e}")

tests_failed += 1

# Test 2: Check that Term2_TTM > Term1_TTM for all rows

try:

assert all(combined_spreads['Term2_TTM'] > combined_spreads['Term1_TTM']), "Term2 TTM should always be greater than Term1 TTM"

print(f"Test 2 Passed: Term2 TTM is always greater than Term1 TTM")

tests_passed += 1

except AssertionError as e:

print(f"Test 2 Failed: {e}")

tests_failed += 1

# Test 3: Check that all TTM values are reasonable (positive and typically under 365 days)

try:

assert all(combined_spreads['Term1_TTM'] > 0), "Term1 TTM should be positive"

assert all(combined_spreads['Term2_TTM'] > 0), "Term2 TTM should be positive"

assert combined_spreads['Term1_TTM'].max() < 365, "Term1 TTM should typically be less than 365 days"

assert combined_spreads['Term2_TTM'].max() < 730, "Term2 TTM should typically be less than 730 days"

print(f"Test 3 Passed: TTM values are within reasonable ranges")

tests_passed += 1

except AssertionError as e:

print(f"Test 3 Failed: {e}")

tests_failed += 1

# Test 4: Check for missing values in critical columns

critical_columns = ['Term1_Futures_Price', 'Term2_Futures_Price', 'Term1_TTM', 'Term2_TTM']

try:

for col in critical_columns:

assert combined_spreads[col].isna().sum() == 0, f"Missing values in {col}"

print(f"Test 4 Passed: No missing values in critical columns")

tests_passed += 1

except AssertionError as e:

print(f"Test 4 Failed: {e}")

tests_failed += 1

# Test 5: Check that futures prices are positive

try:

assert all(combined_spreads['Term1_Futures_Price'] > 0), "Term1 futures prices should be positive"

assert all(combined_spreads['Term2_Futures_Price'] > 0), "Term2 futures prices should be positive"

print(f"Test 5 Passed: All futures prices are positive")

tests_passed += 1

except AssertionError as e:

print(f"Test 5 Failed: {e}")

tests_failed += 1

print(f"\nData quality checks complete: {tests_passed} passed, {tests_failed} failed")

return tests_passed, tests_failed

# Run the data quality checks

tests_passed, tests_failed = check_futures_data_quality(combined_spreads)

Running data quality checks on futures data...

Test 1 Passed: All three indices are present

Test 2 Passed: Term2 TTM is always greater than Term1 TTM

Test 3 Failed: Term1 TTM should be positive

Test 4 Passed: No missing values in critical columns

Test 5 Passed: All futures prices are positive

Data quality checks complete: 4 passed, 1 failed

Running data quality checks on futures data...

Test 1 Passed: All three indices are present

Test 2 Passed: Term2 TTM is always greater than Term1 TTM

Test 3 Failed: Term1 TTM should be positive

Test 4 Passed: No missing values in critical columns

Test 5 Passed: All futures prices are positive

Data quality checks complete: 4 passed, 1 failed

Interestingly, we do see a failed test case where TTM for Term 1 was not positive.

# Identify rows where Term1_TTM is not positive

problematic_rows = combined_spreads[combined_spreads['Term1_TTM'] <= 0]

# Display the count of problematic rows

print(f"Found {len(problematic_rows)} rows with non-positive Term1_TTM values")

# Display the problematic rows

if len(problematic_rows) > 0:

print("\nRows with non-positive Term1_TTM values:")

display(problematic_rows)

# Group by index to see distribution of issues

print("\nDistribution by index:")

index_counts = problematic_rows['Index'].value_counts()

display(index_counts)

# Look at the date distribution

print("\nDate range of problematic rows:")

print(f"Earliest: {problematic_rows['Date'].min()}")

print(f"Latest: {problematic_rows['Date'].max()}")

# Check term 2 values for these rows

print("\nTerm2_TTM statistics for these rows:")

print(f"Min: {problematic_rows['Term2_TTM'].min()}")

print(f"Max: {problematic_rows['Term2_TTM'].max()}")

print(f"Mean: {problematic_rows['Term2_TTM'].mean()}")

# See if we can identify a pattern

print("\nSample of original contract specifications for these rows:")

display(problematic_rows[['Date', 'Index', 'Term1_ContractSpec', 'Term1_SettlementDate', 'Term1_TTM']].head(10))

Found 180 rows with non-positive Term1_TTM values

Rows with non-positive Term1_TTM values:

| Date | Term1_Futures_Price | Term1_Volume | Term1_OpenInterest | Term1_ContractSpec | Term1_SettlementDate | Term1_TTM | Term2_Futures_Price | Term2_Volume | Term2_OpenInterest | Term2_ContractSpec | Term2_SettlementDate | Term2_TTM | Index | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 52 | 2010-03-19 | 1172.95 | 57789.0 | NaN | MAR 10 | 2010-03-19 | 0.0 | 1156.25 | 2165610.0 | 2364398.0 | JUN 10 | 2010-06-18 | 91.0 | SPX |

| 115 | 2010-06-18 | 1118.83 | 58546.0 | NaN | JUN 10 | 2010-06-18 | 0.0 | 1110.25 | 1630832.0 | 2533026.0 | SEP 10 | 2010-09-17 | 91.0 | SPX |

| 178 | 2010-09-17 | 1133.00 | 74961.0 | NaN | SEP 10 | 2010-09-17 | 0.0 | 1119.75 | 1929510.0 | 2436902.0 | DEC 10 | 2010-12-17 | 91.0 | SPX |

| 242 | 2010-12-17 | 1242.35 | 47534.0 | NaN | DEC 10 | 2010-12-17 | 0.0 | 1238.50 | 1338470.0 | 2392696.0 | MAR 11 | 2011-03-18 | 91.0 | SPX |

| 304 | 2011-03-18 | 1291.00 | 90105.0 | NaN | MAR 11 | 2011-03-18 | 0.0 | 1274.25 | 2335018.0 | 2565944.0 | JUN 11 | 2011-06-17 | 91.0 | SPX |

| ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... | ... |

| 11080 | 2023-12-15 | 36996.45 | 3063.0 | 28709.0 | DEC 23 | 2023-12-15 | 0.0 | 37661.00 | 158088.0 | 93658.0 | MAR 24 | 2024-03-15 | 91.0 | INDU |

| 11141 | 2024-03-15 | 38691.18 | 1475.0 | 21587.0 | MAR 24 | 2024-03-15 | 0.0 | 39153.00 | 168986.0 | 92119.0 | JUN 24 | 2024-06-21 | 98.0 | INDU |

| 11208 | 2024-06-21 | 39261.95 | 910.0 | 27512.0 | JUN 24 | 2024-06-21 | 0.0 | 39583.00 | 120696.0 | 79168.0 | SEP 24 | 2024-09-20 | 91.0 | INDU |

| 11271 | 2024-09-20 | 41946.09 | 1513.0 | 13934.0 | SEP 24 | 2024-09-20 | 0.0 | 42443.00 | 114933.0 | 84305.0 | DEC 24 | 2024-12-20 | 91.0 | INDU |

| 11335 | 2024-12-20 | 42197.66 | 2504.0 | 20986.0 | DEC 24 | 2024-12-20 | 0.0 | 43316.00 | 161904.0 | 83805.0 | MAR 25 | 2025-03-21 | 91.0 | INDU |

180 rows × 14 columns

Distribution by index:

Index

SPX 60

NDX 60

INDU 60

Name: count, dtype: int64

Date range of problematic rows:

Earliest: 2010-03-19 00:00:00

Latest: 2024-12-20 00:00:00

Term2_TTM statistics for these rows:

Min: 84.0

Max: 98.0

Mean: 91.35

Sample of original contract specifications for these rows:

| Date | Index | Term1_ContractSpec | Term1_SettlementDate | Term1_TTM | |

|---|---|---|---|---|---|

| 52 | 2010-03-19 | SPX | MAR 10 | 2010-03-19 | 0.0 |

| 115 | 2010-06-18 | SPX | JUN 10 | 2010-06-18 | 0.0 |

| 178 | 2010-09-17 | SPX | SEP 10 | 2010-09-17 | 0.0 |

| 242 | 2010-12-17 | SPX | DEC 10 | 2010-12-17 | 0.0 |

| 304 | 2011-03-18 | SPX | MAR 11 | 2011-03-18 | 0.0 |

| 367 | 2011-06-17 | SPX | JUN 11 | 2011-06-17 | 0.0 |

| 430 | 2011-09-16 | SPX | SEP 11 | 2011-09-16 | 0.0 |

| 494 | 2011-12-16 | SPX | DEC 11 | 2011-12-16 | 0.0 |

| 555 | 2012-03-16 | SPX | MAR 12 | 2012-03-16 | 0.0 |

| 619 | 2012-06-15 | SPX | JUN 12 | 2012-06-15 | 0.0 |

After Analysis, we note that there are rows in the dataset for SPX index where the TTM was 0, corresponding to some of the rollover dates. We will resolve this in the code dowstream by adding these code blocks when merging:

dt = merged_df[ttm2] - merged_df[ttm1] merged_df[f”cal_{index_code}_rf”] = np.where( dt > 0, 100.0 * merged_df[“implied_forward_raw”] * (360.0 / dt), np.nan )

merged_df[f”ois_fwd_{index_code}”] = np.where( dt > 0, merged_df[“ois_fwd_raw”] * (360.0 / dt) * 100.0, np.nan )

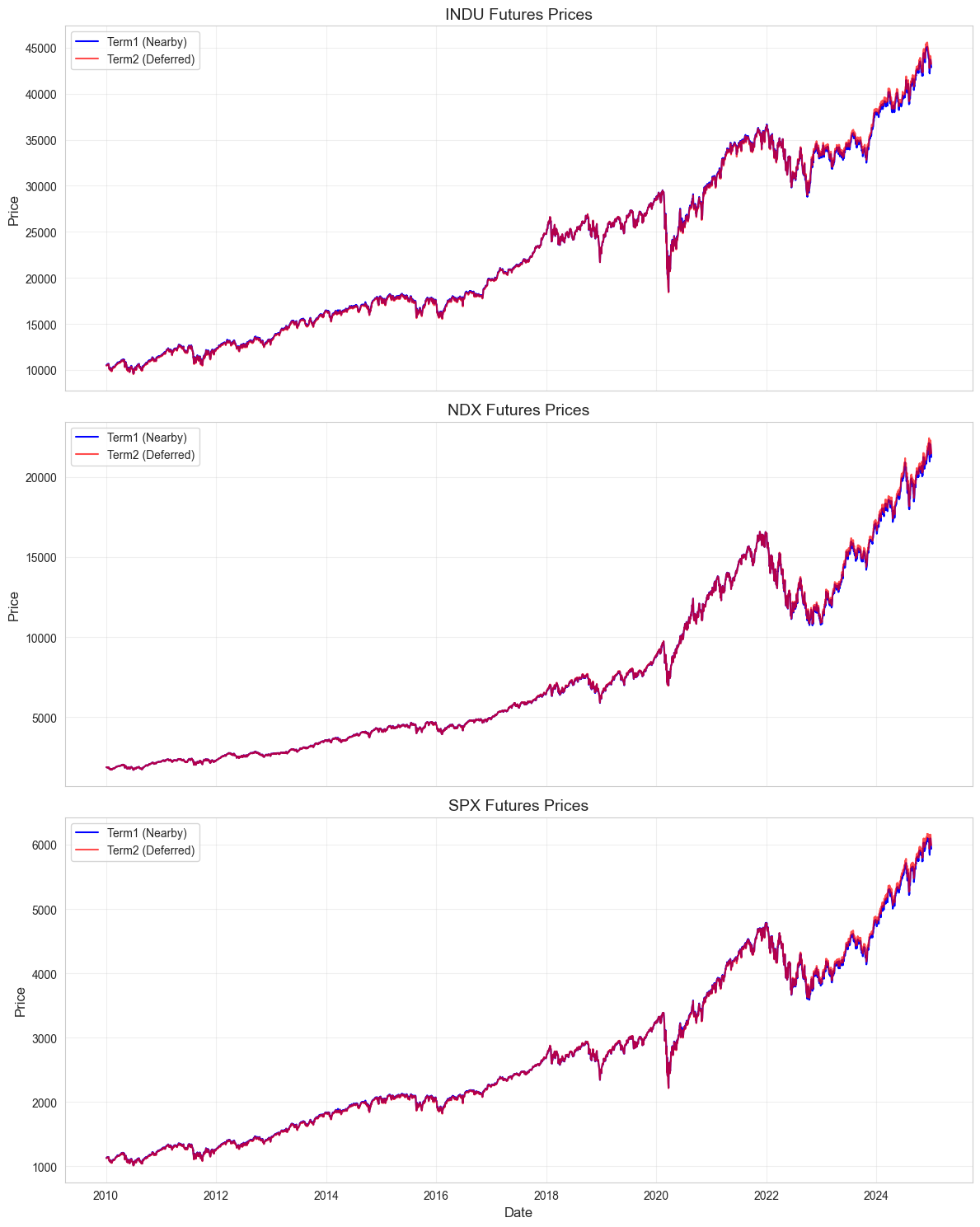

Futures Price Visualization#

Let’s visualize the futures prices for Term1 and Term2 for each index:

# Set up a multi-panel figure

fig, axes = plt.subplots(3, 1, figsize=(12, 15), sharex=True)

indices = sorted(combined_spreads['Index'].unique())

for i, index in enumerate(indices):

index_df = combined_spreads[combined_spreads['Index'] == index]

# Plot Term1 and Term2 prices

axes[i].plot(index_df['Date'], index_df['Term1_Futures_Price'], 'b-', label='Term1 (Nearby)')

axes[i].plot(index_df['Date'], index_df['Term2_Futures_Price'], 'r-', alpha=0.7, label='Term2 (Deferred)')

axes[i].set_title(f'{index} Futures Prices', fontsize=14)

axes[i].set_ylabel('Price', fontsize=12)

axes[i].grid(True, alpha=0.3)

axes[i].legend(loc='upper left')

# Set common labels

axes[2].set_xlabel('Date', fontsize=12)

plt.tight_layout()

# Save the visualization

plt.savefig(OUTPUT_DIR / 'futures_prices_by_index.png', dpi=300)

plt.show()

Integration with Forward Rate Calculations#

The processed futures data is now ready for integration with the OIS rates data to calculate implied forward rates and arbitrage spreads.

The key outputs from this processing pipeline include:

Individual Index Calendar Spreads: Saved as CSV files (

SPX_Calendar_spread.csv,NDX_Calendar_spread.csv,INDU_Calendar_spread.csv) in thePROCESSED_DIR.Combined Calendar Spreads: Saved as

all_indices_calendar_spreads.csvin thePROCESSED_DIR.

These files contain the following critical information:

Term1_Futures_Price and Term2_Futures_Price: Prices for the nearby and deferred futures contracts

Term1_SettlementDate and Term2_SettlementDate: Settlement dates for each contract

Term1_TTM and Term2_TTM: Time-to-maturity in days

In the next step, these files will be used along with the processed OIS rates to calculate:

Futures-implied forward rates

OIS-implied forward rates

Equity spot-futures arbitrage spreads

The accurate processing of settlement dates and TTM is crucial for properly aligning the futures contracts with OIS rates and accumulating dividends over the correct time periods.