Equity Spot-Futures Arbitrage: Implied Forward Rate Computation#

This notebook demonstrates how to compute implied forward rates from equity index futures, mirroring the approach of Hazelkorn et al. (2021). Our goal is to construct:

where

and

The difference between the futures-implied forward rate and the 3-month OIS rate can reveal potential funding frictions or other market constraints that prevent perfect spot-futures arbitrage in equity markets.

import pandas as pd

import numpy as np

from datetime import datetime, timedelta

import calendar

import logging

import sys

import os

import matplotlib.pyplot as plt

import seaborn as sns

from pathlib import Path

%matplotlib inline

sns.set_style('whitegrid')

# Add the src directory to the path to import our settings

sys.path.insert(1, "./src")

try:

from settings import config

print("Successfully imported config from settings module")

except ImportError:

print("Failed to import config. Using local fallback.")

def config(key):

config_dict = {

"DATA_DIR": Path("./_data"),

"TEMP_DIR": Path("./_data/temp"),

"INPUT_DIR": Path("./_data/input"),

"PROCESSED_DIR": Path("./_data/processed"),

"MANUAL_DATA_DIR": Path("./data_manual"),

"OUTPUT_DIR": Path("./_output"),

"START_DATE": "2010-01-01",

"END_DATE": "2025-01-01"

}

return config_dict.get(key, Path("./data"))

# Basic paths

DATA_DIR = config("DATA_DIR")

TEMP_DIR = config("TEMP_DIR")

INPUT_DIR = config("INPUT_DIR")

PROCESSED_DIR = config("PROCESSED_DIR")

DATA_MANUAL = config("MANUAL_DATA_DIR")

OUTPUT_DIR = config("OUTPUT_DIR")

START_DATE = pd.to_datetime(config("START_DATE"))

END_DATE = pd.to_datetime(config("END_DATE"))

print(f"DATA_DIR = {DATA_DIR}")

print(f"PROCESSED_DIR = {PROCESSED_DIR}")

print(f"START_DATE = {START_DATE.date()}, END_DATE = {END_DATE.date()}")

INDEX_CODES = ["SPX", "NDX", "INDU"]

Successfully imported config from settings module

DATA_DIR = C:\Users\Andik\OneDrive\Desktop\Chicago\Full_stack_QF\Equity_Spot_futures_arb\_data

PROCESSED_DIR = C:\Users\Andik\OneDrive\Desktop\Chicago\Full_stack_QF\Equity_Spot_futures_arb\_data\processed

START_DATE = 2010-01-01, END_DATE = 2024-12-31

Theoretical Background#

In classical spot-futures parity for an equity index (S_t) that pays dividends from (t) to (t + \tau), the no-arbitrage futures price is:

However, a direct spot vs. futures comparison can be noisy if they close at different times (e.g., 4:00 pm vs. 4:15 pm). Instead, we look at two futures contracts (maturing at (\tau_1) and (\tau_2)):

to isolate the implied forward rate (f_{t,\tau_1,\tau_2}). We then define the Equity Spot-Futures Arbitrage Spread as:

A positive (\text{ESF}_t) indicates the implied equity forward rate is higher than the OIS benchmark, potentially signaling a funding-cost wedge or other limits to arbitrage.

def build_daily_dividends(index_code: str) -> pd.DataFrame:

"""

Load daily dividends for the given index code from bloomberg_historical_data.parquet.

Return columns: [Date, Daily_Div].

"""

print(f"[{index_code}] Building daily dividend table")

input_file = Path(INPUT_DIR) / "bloomberg_historical_data.parquet"

if not os.path.exists(input_file):

print("Primary input file not found, switching to cached data")

input_file = Path(DATA_MANUAL) / "bloomberg_historical_data.parquet"

raw_df = pd.read_parquet(input_file)

div_col = (f"{index_code} Index", "INDX_GROSS_DAILY_DIV")

if div_col not in raw_df.columns:

raise ValueError(f"Missing daily dividend column {div_col} for index={index_code}")

div_df = raw_df.loc[:, div_col].to_frame("Daily_Div").reset_index()

div_df.rename(columns={"index": "Date"}, inplace=True)

div_df["Date"] = pd.to_datetime(div_df["Date"], errors="coerce")

div_df["Daily_Div"] = div_df["Daily_Div"].fillna(0)

# Optionally drop any row that has no valid date

before_drop = len(div_df)

div_df.dropna(subset=["Date"], inplace=True)

after_drop = len(div_df)

if after_drop < before_drop:

print(f"[{index_code}] Dropped {before_drop - after_drop} rows with invalid or missing date in daily_div.")

div_df.sort_values("Date", inplace=True)

div_df.reset_index(drop=True, inplace=True)

print(f"[{index_code}] daily dividends final shape: {div_df.shape}")

print(f"[{index_code}] Sample daily dividends:\n{div_df.head(10)}")

return div_df

def barndorff_nielsen_filter(df: pd.DataFrame,

colname: str,

date_col: str = "Date",

window: int = 45,

threshold: float = 10.0) -> pd.DataFrame:

"""

Barndorff-Nielsen outlier filter on 'colname' over ±window days.

1) rolling median => ...

2) abs_dev from that median

3) rolling mean(abs_dev) => mad

4) outlier if abs_dev/mad >= threshold => set colname_filtered=NaN

"""

df = df.sort_values(date_col).copy()

rolling_median = df[colname].rolling(window=window*2+1, center=True, min_periods=1).median()

rolling_median_shifted = rolling_median.shift(1)

df["abs_dev"] = (df[colname] - rolling_median_shifted).abs()

rolling_mad = df["abs_dev"].rolling(window=window*2+1, center=True, min_periods=1).mean()

rolling_mad_shifted = rolling_mad.shift(1)

df["bad_price"] = (df["abs_dev"] / rolling_mad_shifted) >= threshold

df.loc[df[colname].isna(), "bad_price"] = False

# Count how many outliers

outlier_count = df["bad_price"].sum()

if outlier_count > 0:

print(f"Barndorff-Nielsen filter: flagged {int(outlier_count)} outliers in {colname}")

df[f"{colname}_filtered"] = df[colname].where(~df["bad_price"], np.nan)

df.drop(["abs_dev", "bad_price"], axis=1, inplace=True, errors="ignore")

return df

def process_index_forward_rates(index_code: str) -> pd.DataFrame:

"""

1) Load near/next futures for index_code from _Calendar_spread.csv

2) Merge with single OIS_3M (as-of)

3) Merge daily dividends, compute Div_Sum1_Comp & Div_Sum2_Comp

4) Implied forward => cal_{index_code}_rf, OIS forward => ois_fwd_{index_code}, spread

5) Barndorff outlier filter, then multiply spread by 100 => bps

6) Return the DataFrame

"""

print(f"[{index_code}] Starting forward rate computation")

fut_file = Path(PROCESSED_DIR) / f"{index_code}_Calendar_spread.csv"

if not fut_file.exists():

print(f"[{index_code}] Missing futures file: {fut_file}")

return pd.DataFrame()

fut_df = pd.read_csv(fut_file)

print(f"[{index_code}] Loaded futures shape: {fut_df.shape}")

if "Date" not in fut_df.columns:

print(f"[{index_code}] No 'Date' column in {fut_file}, aborting.")

return pd.DataFrame()

fut_df["Date"] = pd.to_datetime(fut_df["Date"], errors="coerce")

before_drop = len(fut_df)

fut_df.dropna(subset=["Date"], inplace=True)

print(f"[{index_code}] Dropped {before_drop - len(fut_df)} rows lacking a valid Date in futures.")

fut_df["Term1_SettlementDate"] = pd.to_datetime(fut_df["Term1_SettlementDate"], errors="coerce")

fut_df["Term2_SettlementDate"] = pd.to_datetime(fut_df["Term2_SettlementDate"], errors="coerce")

fut_df.sort_values("Date", inplace=True)

fut_df.reset_index(drop=True, inplace=True)

# === Merge single OIS_3M

ois_file = Path(PROCESSED_DIR) / "cleaned_ois_rates.csv"

if not ois_file.exists():

print(f"[{index_code}] Missing OIS file: {ois_file}")

return pd.DataFrame()

ois_df = pd.read_csv(ois_file)

if "Date" not in ois_df.columns:

ois_df.rename(columns={"Unnamed: 0": "Date"}, inplace=True)

ois_df["Date"] = pd.to_datetime(ois_df["Date"], errors="coerce")

ois_df.sort_values("Date", inplace=True)

# as-of merge

prev_len = len(fut_df)

merged_df = pd.merge_asof(

fut_df, ois_df, on="Date", direction="backward"

)

after_len = len(merged_df)

print(f"[{index_code}] as-of merged OIS: from {prev_len} -> {after_len} rows (should be same).")

# rename OIS_3M => 'OIS'

if "OIS_3M" in merged_df.columns:

merged_df.rename(columns={"OIS_3M": "OIS"}, inplace=True)

else:

print(f"[{index_code}] 'OIS_3M' column not found in OIS data, using default 'OIS_3M'?")

# === Load daily dividends

div_df = build_daily_dividends(index_code)

# add cumsum in div_df

div_df["CumDiv"] = div_df["Daily_Div"].cumsum()

# merge cumsum at current date

prev_len = len(merged_df)

merged_df = pd.merge_asof(

merged_df.sort_values("Date"),

div_df[["Date", "CumDiv"]].sort_values("Date"),

on="Date",

direction="backward"

)

after_len = len(merged_df)

print(

f"[{index_code}] as-of merged CumDiv at current date: from {prev_len} -> {after_len} rows."

)

merged_df.rename(columns={"CumDiv": "CumDiv_current"}, inplace=True)

print(f"[{index_code}] Sample merged rows with cumulative div:\n{merged_df.head(10)}")

# same approach for Term1 & Term2

t1_df = div_df.rename(columns={"Date": "Term1_SettlementDate", "CumDiv": "CumDiv_Term1"})

prev_len = len(merged_df)

merged_df = pd.merge_asof(

merged_df.sort_values("Term1_SettlementDate"),

t1_df.sort_values("Term1_SettlementDate"),

on="Term1_SettlementDate",

direction="backward"

)

after_len = len(merged_df)

print(

f"[{index_code}] as-of merged CumDiv for Term1: from {prev_len} -> {after_len} rows."

)

t2_df = div_df.rename(columns={"Date": "Term2_SettlementDate", "CumDiv": "CumDiv_Term2"})

prev_len = len(merged_df)

merged_df = pd.merge_asof(

merged_df.sort_values("Term2_SettlementDate"),

t2_df.sort_values("Term2_SettlementDate"),

on="Term2_SettlementDate",

direction="backward"

)

after_len = len(merged_df)

print(

f"[{index_code}] as-of merged CumDiv for Term2: from {prev_len} -> {after_len} rows."

)

# compute Div_Sum1 & Div_Sum2

merged_df["Div_Sum1"] = merged_df["CumDiv_Term1"] - merged_df["CumDiv_current"]

merged_df["Div_Sum2"] = merged_df["CumDiv_Term2"] - merged_df["CumDiv_current"]

# Handle missing TTM or price

# If TTM is missing, can't compute rates => drop

before_drop = len(merged_df)

merged_df.dropna(subset=["Term1_TTM", "Term2_TTM", "Term1_Futures_Price", "Term2_Futures_Price"], inplace=True)

print(

f"[{index_code}] Dropped {before_drop - len(merged_df)} rows missing TTM or Futures_Price."

)

# 4) Compounding

ttm1 = "Term1_TTM"

ttm2 = "Term2_TTM"

merged_df["Div_Sum1_Comp"] = merged_df["Div_Sum1"] * (

((merged_df[ttm1] / 2.0) / 360.0) * merged_df["OIS"] + 1.0

)

merged_df["Div_Sum2_Comp"] = merged_df["Div_Sum2"] * (

((merged_df[ttm2] / 2.0) / 360.0) * merged_df["OIS"] + 1.0

)

# Implied Forward

fp1 = "Term1_Futures_Price"

fp2 = "Term2_Futures_Price"

merged_df["implied_forward_raw"] = (

(merged_df[fp2] + merged_df["Div_Sum2_Comp"]) /

(merged_df[fp1] + merged_df["Div_Sum1_Comp"])

- 1.0

)

dt = merged_df[ttm2] - merged_df[ttm1]

merged_df[f"cal_{index_code}_rf"] = np.where(

dt > 0,

100.0 * merged_df["implied_forward_raw"] * (360.0 / dt),

np.nan

)

# OIS-implied forward

merged_df["ois_fwd_raw"] = (

(1.0 + merged_df["OIS"] * merged_df[ttm2] / 360.0) /

(1.0 + merged_df["OIS"] * merged_df[ttm1] / 360.0)

- 1.0

)

merged_df[f"ois_fwd_{index_code}"] = np.where(

dt > 0,

merged_df["ois_fwd_raw"] * (360.0 / dt) * 100.0,

np.nan

)

# Spread

spread_col = f"spread_{index_code}"

merged_df[spread_col] = merged_df[f"cal_{index_code}_rf"] - merged_df[f"ois_fwd_{index_code}"]

# BN outlier filter

merged_df = barndorff_nielsen_filter(merged_df, spread_col, date_col="Date", window=45, threshold=10)

# If outlier => set cal_rf & spread to NaN

out_mask = merged_df[f"{spread_col}_filtered"].isna()

outliers_count = out_mask.sum()

if outliers_count > 0:

print(f"[{index_code}] Setting {outliers_count} outliers to NaN for cal_{index_code}_rf & {spread_col}")

merged_df.loc[out_mask, f"cal_{index_code}_rf"] = np.nan

merged_df.loc[out_mask, spread_col] = np.nan

# Multiply spread by 100 => bps

merged_df[spread_col] = merged_df[spread_col] * 100.0

merged_df.set_index("Date", inplace=True)

print(f"[{index_code}] Final forward rates shape: {merged_df.shape}")

print(

f"[{index_code}] Sample final rows:\n"

+ merged_df[[f"cal_{index_code}_rf", f"ois_fwd_{index_code}", spread_col]].tail(5).to_string()

)

return merged_df

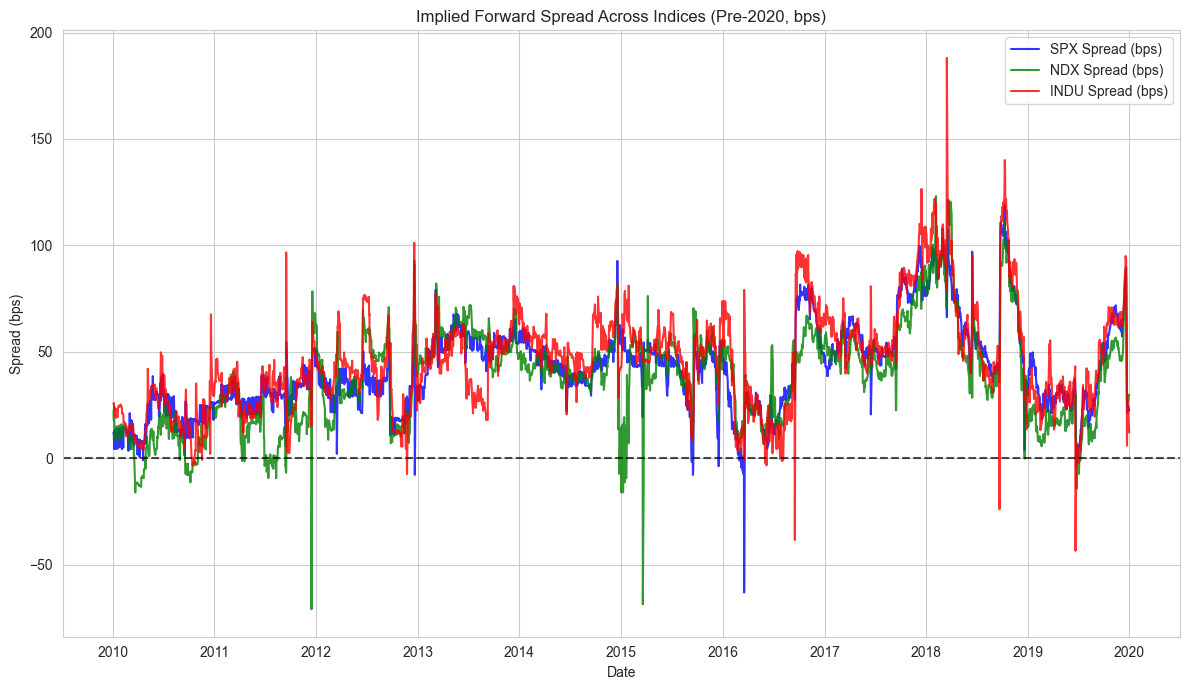

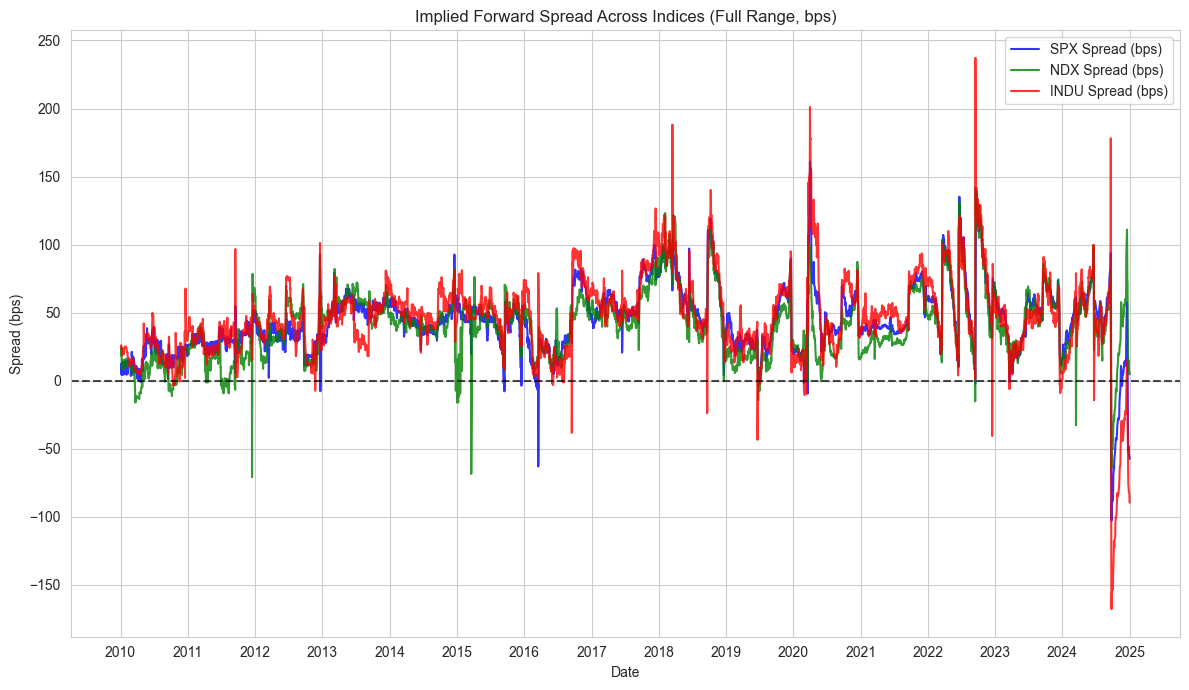

def plot_all_indices(results: dict, keep_dates: bool = True):

"""

Generate two charts for each index's final spread_{idx} in basis points:

1. From START_DATE to 2020-01-01

2. From START_DATE to END_DATE (full range)

By default (keep_dates=True), we reindex to the union of all dates to keep the

X-axis from skipping days that are missing in some index.

If you want to only show existing dates in each index's data, set keep_dates=False.

"""

# Define date ranges

pre_2020_end = pd.to_datetime('2020-01-01')

# If keep_dates: find the union of all dates across all DataFrames

if keep_dates:

all_dates = set()

for idx, df in results.items():

if df is not None and not df.empty:

all_dates.update(df.index.tolist())

# Build a sorted list

date_index = pd.to_datetime(sorted(all_dates))

else:

date_index = None

colors = {"SPX": "blue", "NDX": "green", "INDU": "red"}

# Create Figure 1: START_DATE to 2020-01-01

plt.figure(figsize=(12, 7))

for idx, df in results.items():

if df is not None and not df.empty:

spread_col = f"spread_{idx}"

# Filter to pre-2020 data

pre_2020_df = df[df.index <= pre_2020_end]

# If empty after filtering, skip

if pre_2020_df.empty:

continue

# reindex if desired

if keep_dates and date_index is not None:

filtered_dates = date_index[date_index <= pre_2020_end]

df_plot = pre_2020_df.reindex(filtered_dates).ffill() # Forward fill missing values

else:

df_plot = pre_2020_df

plt.plot(

df_plot.index,

df_plot[spread_col],

color=colors.get(idx, "black"),

alpha=0.8,

label=f"{idx} Spread (bps)"

)

plt.axhline(0, color="k", linestyle="--", alpha=0.7)

plt.title("Implied Forward Spread Across Indices (Pre-2020, bps)")

plt.xlabel("Date")

plt.ylabel("Spread (bps)")

plt.legend()

plt.grid(True)

plt.tight_layout()

ax = plt.gca()

ax.xaxis.set_major_locator(plt.matplotlib.dates.YearLocator())

ax.xaxis.set_major_formatter(plt.matplotlib.dates.DateFormatter("%Y"))

# Display the first plot

plt.show()

# Create Figure 2: START_DATE to END_DATE (full range)

plt.figure(figsize=(12, 7))

for idx, df in results.items():

if df is not None and not df.empty:

spread_col = f"spread_{idx}"

# reindex if desired

if keep_dates and date_index is not None:

df_plot = df.reindex(date_index).ffill() # Forward fill missing values

else:

df_plot = df

plt.plot(

df_plot.index,

df_plot[spread_col],

color=colors.get(idx, "black"),

alpha=0.8,

label=f"{idx} Spread (bps)"

)

plt.axhline(0, color="k", linestyle="--", alpha=0.7)

plt.title("Implied Forward Spread Across Indices (Full Range, bps)")

plt.xlabel("Date")

plt.ylabel("Spread (bps)")

plt.legend()

plt.grid(True)

plt.tight_layout()

ax = plt.gca()

ax.xaxis.set_major_locator(plt.matplotlib.dates.YearLocator())

ax.xaxis.set_major_formatter(plt.matplotlib.dates.DateFormatter("%Y"))

# Display the second plot

plt.show()

def main():

print("== Starting forward rate calculations with compounding dividends, single OIS, BN outlier filter ==")

results = {}

for idx in INDEX_CODES:

df_res = process_index_forward_rates(idx)

results[idx] = df_res

# Create both plots

plot_all_indices(results, keep_dates=True)

print("All computations completed successfully.")

# Execute the main function

if __name__ == "__main__":

main()

== Starting forward rate calculations with compounding dividends, single OIS, BN outlier filter ==

[SPX] Starting forward rate computation

[SPX] Loaded futures shape: (3781, 14)

[SPX] Dropped 0 rows lacking a valid Date in futures.

[SPX] as-of merged OIS: from 3781 -> 3781 rows (should be same).

[SPX] Building daily dividend table

Primary input file not found, switching to cached data

[SPX] daily dividends final shape: (3913, 2)

[SPX] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.058362

2 2010-01-05 0.001744

3 2010-01-06 0.497980

4 2010-01-07 0.061819

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.113508

9 2010-01-14 0.021957

[SPX] as-of merged CumDiv at current date: from 3781 -> 3781 rows.

[SPX] Sample merged rows with cumulative div:

Date Term1_Futures_Price Term1_Volume Term1_OpenInterest \

0 2010-01-04 1128.75 1282633.0 2440458.0

1 2010-01-05 1132.25 1368386.0 2402850.0

2 2010-01-06 1133.00 1252015.0 2396493.0

3 2010-01-07 1137.50 1553963.0 2406352.0

4 2010-01-08 1141.50 1508175.0 2758348.0

5 2010-01-11 1142.50 1444997.0 2427453.0

6 2010-01-12 1134.00 2089364.0 2439036.0

7 2010-01-13 1141.50 2110033.0 2475322.0

8 2010-01-14 1145.25 1346436.0 2473392.0

9 2010-01-15 1132.25 2031715.0 2454453.0

Term1_ContractSpec Term1_SettlementDate Term1_TTM Term2_Futures_Price \

0 MAR 10 2010-03-19 74.0 1124.00

1 MAR 10 2010-03-19 73.0 1127.50

2 MAR 10 2010-03-19 72.0 1128.00

3 MAR 10 2010-03-19 71.0 1132.50

4 MAR 10 2010-03-19 70.0 1136.75

5 MAR 10 2010-03-19 67.0 1137.50

6 MAR 10 2010-03-19 66.0 1129.00

7 MAR 10 2010-03-19 65.0 1136.75

8 MAR 10 2010-03-19 64.0 1140.25

9 MAR 10 2010-03-19 63.0 1127.50

Term2_Volume Term2_OpenInterest Term2_ContractSpec Term2_SettlementDate \

0 1641.0 3354.0 JUN 10 2010-06-18

1 686.0 3432.0 JUN 10 2010-06-18

2 1163.0 3713.0 JUN 10 2010-06-18

3 1135.0 4154.0 JUN 10 2010-06-18

4 1080.0 17466.0 JUN 10 2010-06-18

5 419.0 4638.0 JUN 10 2010-06-18

6 481.0 4765.0 JUN 10 2010-06-18

7 1174.0 5389.0 JUN 10 2010-06-18

8 333.0 5357.0 JUN 10 2010-06-18

9 1432.0 5936.0 JUN 10 2010-06-18

Term2_TTM Index OIS CumDiv_current

0 165.0 SPX 0.001620 0.058362

1 164.0 SPX 0.001550 0.060106

2 163.0 SPX 0.001460 0.558086

3 162.0 SPX 0.001450 0.619905

4 161.0 SPX 0.001430 0.619905

5 158.0 SPX 0.001430 0.619905

6 157.0 SPX 0.001415 0.619905

7 156.0 SPX 0.001470 0.733413

8 155.0 SPX 0.001430 0.755370

9 154.0 SPX 0.001380 0.799620

[SPX] as-of merged CumDiv for Term1: from 3781 -> 3781 rows.

[SPX] as-of merged CumDiv for Term2: from 3781 -> 3781 rows.

[SPX] Dropped 0 rows missing TTM or Futures_Price.

Barndorff-Nielsen filter: flagged 47 outliers in spread_SPX

[SPX] Setting 47 outliers to NaN for cal_SPX_rf & spread_SPX

[SPX] Final forward rates shape: (3781, 29)

[SPX] Sample final rows:

cal_SPX_rf ois_fwd_SPX spread_SPX

Date

2024-12-24 3.778583 4.287412 -50.882869

2024-12-26 3.796641 4.277498 -48.085749

2024-12-27 3.741256 4.277624 -53.636841

2024-12-30 3.717731 4.275913 -55.818186

2024-12-31 3.698950 4.274017 -57.506667

[NDX] Starting forward rate computation

[NDX] Loaded futures shape: (3781, 14)

[NDX] Dropped 0 rows lacking a valid Date in futures.

[NDX] as-of merged OIS: from 3781 -> 3781 rows (should be same).

[NDX] Building daily dividend table

Primary input file not found, switching to cached data

[NDX] daily dividends final shape: (3913, 2)

[NDX] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.148515

2 2010-01-05 0.000000

3 2010-01-06 0.000000

4 2010-01-07 0.000000

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.000000

9 2010-01-14 0.113752

[NDX] as-of merged CumDiv at current date: from 3781 -> 3781 rows.

[NDX] Sample merged rows with cumulative div:

Date Term1_Futures_Price Term1_Volume Term1_OpenInterest \

0 2010-01-04 1886.75 204140.0 314877.0

1 2010-01-05 1885.25 207245.0 309080.0

2 2010-01-06 1878.50 259627.0 310532.0

3 2010-01-07 1877.50 239907.0 317226.0

4 2010-01-08 1890.00 267314.0 379994.0

5 2010-01-11 1883.50 243454.0 314557.0

6 2010-01-12 1865.50 326600.0 306114.0

7 2010-01-13 1882.50 312998.0 331168.0

8 2010-01-14 1888.25 204465.0 324274.0

9 2010-01-15 1862.25 343007.0 320266.0

Term1_ContractSpec Term1_SettlementDate Term1_TTM Term2_Futures_Price \

0 MAR 10 2010-03-19 74.0 1884.75

1 MAR 10 2010-03-19 73.0 1883.00

2 MAR 10 2010-03-19 72.0 1876.50

3 MAR 10 2010-03-19 71.0 1875.00

4 MAR 10 2010-03-19 70.0 1887.25

5 MAR 10 2010-03-19 67.0 1880.75

6 MAR 10 2010-03-19 66.0 1862.75

7 MAR 10 2010-03-19 65.0 1879.75

8 MAR 10 2010-03-19 64.0 1885.50

9 MAR 10 2010-03-19 63.0 1859.75

Term2_Volume Term2_OpenInterest Term2_ContractSpec Term2_SettlementDate \

0 33.0 671.0 JUN 10 2010-06-18

1 74.0 651.0 JUN 10 2010-06-18

2 33.0 665.0 JUN 10 2010-06-18

3 47.0 672.0 JUN 10 2010-06-18

4 1001.0 6163.0 JUN 10 2010-06-18

5 288.0 898.0 JUN 10 2010-06-18

6 311.0 1077.0 JUN 10 2010-06-18

7 710.0 1699.0 JUN 10 2010-06-18

8 784.0 2401.0 JUN 10 2010-06-18

9 272.0 2533.0 JUN 10 2010-06-18

Term2_TTM Index OIS CumDiv_current

0 165.0 NDX 0.001620 0.148515

1 164.0 NDX 0.001550 0.148515

2 163.0 NDX 0.001460 0.148515

3 162.0 NDX 0.001450 0.148515

4 161.0 NDX 0.001430 0.148515

5 158.0 NDX 0.001430 0.148515

6 157.0 NDX 0.001415 0.148515

7 156.0 NDX 0.001470 0.148515

8 155.0 NDX 0.001430 0.262267

9 154.0 NDX 0.001380 0.262267

[NDX] as-of merged CumDiv for Term1: from 3781 -> 3781 rows.

[NDX] as-of merged CumDiv for Term2: from 3781 -> 3781 rows.

[NDX] Dropped 0 rows missing TTM or Futures_Price.

Barndorff-Nielsen filter: flagged 48 outliers in spread_NDX

[NDX] Setting 48 outliers to NaN for cal_NDX_rf & spread_NDX

[NDX] Final forward rates shape: (3781, 29)

[NDX] Sample final rows:

cal_NDX_rf ois_fwd_NDX spread_NDX

Date

2024-12-24 4.341428 4.287412 5.401572

2024-12-26 4.426357 4.277498 14.885916

2024-12-27 4.384662 4.277624 10.703781

2024-12-30 4.322400 4.275913 4.648708

2024-12-31 4.323851 4.274017 4.983391

[INDU] Starting forward rate computation

[INDU] Loaded futures shape: (3780, 14)

[INDU] Dropped 0 rows lacking a valid Date in futures.

[INDU] as-of merged OIS: from 3780 -> 3780 rows (should be same).

[INDU] Building daily dividend table

Primary input file not found, switching to cached data

[INDU] daily dividends final shape: (3913, 2)

[INDU] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.377875

2 2010-01-05 0.000000

3 2010-01-06 6.763957

4 2010-01-07 1.360349

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.000000

9 2010-01-14 0.000000

[INDU] as-of merged CumDiv at current date: from 3780 -> 3780 rows.

[INDU] Sample merged rows with cumulative div:

Date Term1_Futures_Price Term1_Volume Term1_OpenInterest \

0 2010-01-04 10519.0 93770.0 69420.0

1 2010-01-05 10515.0 93287.0 65749.0

2 2010-01-06 10516.0 97172.0 63888.0

3 2010-01-07 10545.0 112280.0 67401.0

4 2010-01-08 10566.0 79925.0 61714.0

5 2010-01-11 10604.0 93891.0 63318.0

6 2010-01-12 10588.0 126885.0 62710.0

7 2010-01-13 10628.0 113576.0 63479.0

8 2010-01-14 10663.0 80520.0 64500.0

9 2010-01-15 10563.0 140591.0 66826.0

Term1_ContractSpec Term1_SettlementDate Term1_TTM Term2_Futures_Price \

0 MAR 10 2010-03-19 74.0 10459.0

1 MAR 10 2010-03-19 73.0 10455.0

2 MAR 10 2010-03-19 72.0 10455.0

3 MAR 10 2010-03-19 71.0 10484.0

4 MAR 10 2010-03-19 70.0 10505.0

5 MAR 10 2010-03-19 67.0 10542.0

6 MAR 10 2010-03-19 66.0 10527.0

7 MAR 10 2010-03-19 65.0 10566.0

8 MAR 10 2010-03-19 64.0 10601.0

9 MAR 10 2010-03-19 63.0 10501.0

Term2_Volume Term2_OpenInterest Term2_ContractSpec Term2_SettlementDate \

0 100.0 175.0 JUN 10 2010-06-18

1 26.0 173.0 JUN 10 2010-06-18

2 157.0 193.0 JUN 10 2010-06-18

3 34.0 180.0 JUN 10 2010-06-18

4 146.0 531.0 JUN 10 2010-06-18

5 45.0 230.0 JUN 10 2010-06-18

6 55.0 234.0 JUN 10 2010-06-18

7 21.0 208.0 JUN 10 2010-06-18

8 11.0 206.0 JUN 10 2010-06-18

9 80.0 221.0 JUN 10 2010-06-18

Term2_TTM Index OIS CumDiv_current

0 165.0 INDU 0.001620 0.377875

1 164.0 INDU 0.001550 0.377875

2 163.0 INDU 0.001460 7.141832

3 162.0 INDU 0.001450 8.502181

4 161.0 INDU 0.001430 8.502181

5 158.0 INDU 0.001430 8.502181

6 157.0 INDU 0.001415 8.502181

7 156.0 INDU 0.001470 8.502181

8 155.0 INDU 0.001430 8.502181

9 154.0 INDU 0.001380 11.676328

[INDU] as-of merged CumDiv for Term1: from 3780 -> 3780 rows.

[INDU] as-of merged CumDiv for Term2: from 3780 -> 3780 rows.

[INDU] Dropped 0 rows missing TTM or Futures_Price.

Barndorff-Nielsen filter: flagged 43 outliers in spread_INDU

[INDU] Setting 43 outliers to NaN for cal_INDU_rf & spread_INDU

[INDU] Final forward rates shape: (3780, 29)

[INDU] Sample final rows:

cal_INDU_rf ois_fwd_INDU spread_INDU

Date

2024-12-24 3.525951 4.287412 -76.146147

2024-12-26 3.485142 4.277498 -79.235563

2024-12-27 3.459165 4.277624 -81.845864

2024-12-30 3.446690 4.275913 -82.922307

2024-12-31 3.377212 4.274017 -89.680496

All computations completed successfully.

Exploring the Functions: Visual Understanding of Implied Forward Rate Calculation#

This notebook provides a step-by-step exploration of each function in the implied forward rate calculation process, with visualizations and tables to help build intuition about what’s happening at each stage.

Data loading and preprocessing

Daily dividend accumulation

Barndorff-Nielsen outlier filtering mechanism

The forward rate calculation process

Visualization of results

Let’s break down each component visually to understand the theory.

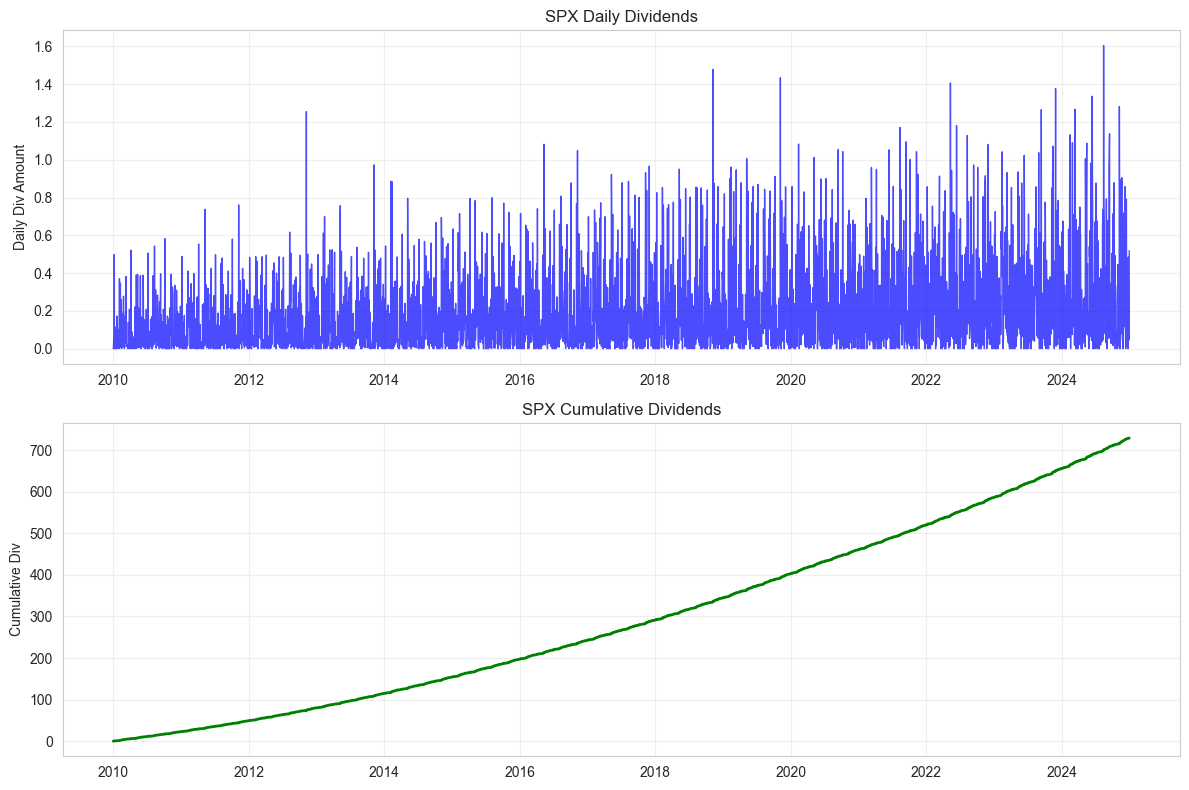

# Function to visualize and explain daily dividends

def explore_daily_dividends(index_code="SPX"):

"""

Explore and visualize how the daily dividend function works

"""

print(f"=== Exploring build_daily_dividends for {index_code} ===")

# Load the data

input_file = Path(INPUT_DIR) / "bloomberg_historical_data.parquet"

if not input_file.exists():

input_file = Path(DATA_MANUAL) / "bloomberg_historical_data.parquet"

if not input_file.exists():

print("No Bloomberg data file found. Cannot proceed with exploration.")

return None

# Load raw data

raw_df = pd.read_parquet(input_file)

# Show the structure of the raw dataframe

print("\nRaw Bloomberg data structure:")

print(f"Shape: {raw_df.shape}")

print("Column structure (MultiIndex):")

print(raw_df.columns[:10]) # Show first 10 columns

# Extract dividend column

div_col = (f"{index_code} Index", "INDX_GROSS_DAILY_DIV")

if div_col not in raw_df.columns:

print(f"Missing dividend column for {index_code}. Trying a different approach...")

# Try to find any dividend-related columns

div_cols = [col for col in raw_df.columns if 'DIV' in str(col)]

if div_cols:

print(f"Found potential dividend columns: {div_cols}")

div_col = div_cols[0]

else:

print("No dividend columns found in the data.")

return None

# Process dividends as in the original function

div_df = raw_df.loc[:, div_col].to_frame("Daily_Div").reset_index()

div_df.rename(columns={"index": "Date"}, inplace=True)

div_df["Date"] = pd.to_datetime(div_df["Date"], errors="coerce")

div_df["Daily_Div"] = div_df["Daily_Div"].fillna(0)

div_df.dropna(subset=["Date"], inplace=True)

div_df.sort_values("Date", inplace=True)

div_df.reset_index(drop=True, inplace=True)

# Create cumulative sum column

div_df["CumDiv"] = div_df["Daily_Div"].cumsum()

# Display processed data

print("\nProcessed dividend data (first 5 rows):")

display(div_df.head())

# Visualize daily dividends

plt.figure(figsize=(12, 8))

# Subplot 1: Daily dividends over time

plt.subplot(2, 1, 1)

plt.plot(div_df["Date"], div_df["Daily_Div"], 'b-', alpha=0.7, linewidth=1)

plt.title(f"{index_code} Daily Dividends")

plt.ylabel("Daily Div Amount")

plt.grid(True, alpha=0.3)

# Subplot 2: Cumulative dividends

plt.subplot(2, 1, 2)

plt.plot(div_df["Date"], div_df["CumDiv"], 'g-', linewidth=2)

plt.title(f"{index_code} Cumulative Dividends")

plt.ylabel("Cumulative Div")

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

# Summary statistics

print("\nDividend Data Summary:")

summary = div_df["Daily_Div"].describe()

display(summary)

# Show time periods with zero and non-zero dividends

zero_div = div_df[div_df["Daily_Div"] == 0].shape[0]

total = div_df.shape[0]

print(f"Days with zero dividends: {zero_div} ({zero_div/total:.1%} of total)")

print(f"Days with non-zero dividends: {total - zero_div} ({(total-zero_div)/total:.1%} of total)")

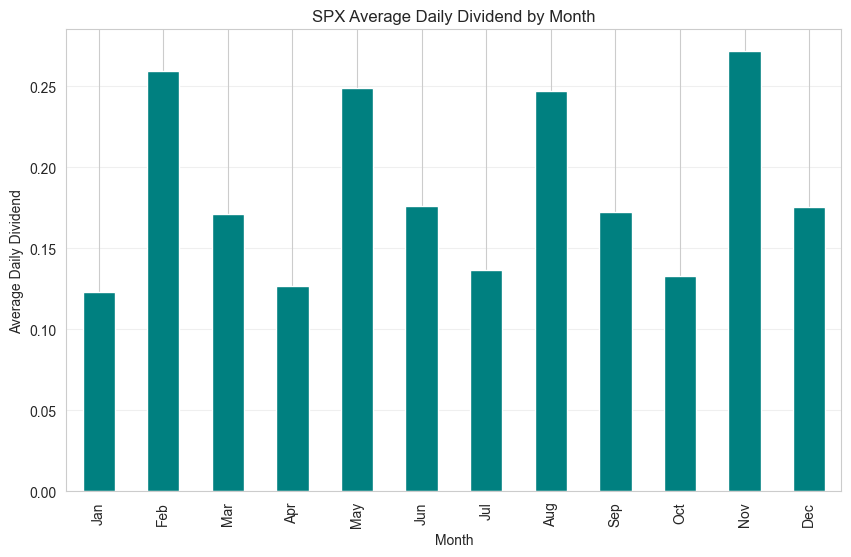

# Monthly dividend patterns (Useful to see if there are dividend seasons)

div_df['month'] = div_df['Date'].dt.month

div_df['year'] = div_df['Date'].dt.year

monthly_pattern = div_df.groupby('month')['Daily_Div'].mean()

plt.figure(figsize=(10, 6))

monthly_pattern.plot(kind='bar', color='teal')

plt.title(f"{index_code} Average Daily Dividend by Month")

plt.xlabel("Month")

plt.ylabel("Average Daily Dividend")

plt.xticks(range(12), ['Jan', 'Feb', 'Mar', 'Apr', 'May', 'Jun', 'Jul', 'Aug', 'Sep', 'Oct', 'Nov', 'Dec'])

plt.grid(True, alpha=0.3, axis='y')

plt.show()

return div_df

# Run the exploration

spx_div_df = explore_daily_dividends("SPX")

=== Exploring build_daily_dividends for SPX ===

Raw Bloomberg data structure:

Shape: (3913, 62)

Column structure (MultiIndex):

MultiIndex([( 'SPX Index', 'PX_LAST'),

( 'SPX Index', 'IDX_EST_DVD_YLD'),

( 'SPX Index', 'INDX_GROSS_DAILY_DIV'),

( 'NDX Index', 'PX_LAST'),

( 'NDX Index', 'IDX_EST_DVD_YLD'),

( 'NDX Index', 'INDX_GROSS_DAILY_DIV'),

('INDU Index', 'PX_LAST'),

('INDU Index', 'IDX_EST_DVD_YLD'),

('INDU Index', 'INDX_GROSS_DAILY_DIV'),

( 'ES1 Index', 'PX_LAST')],

)

Processed dividend data (first 5 rows):

| Date | Daily_Div | CumDiv | |

|---|---|---|---|

| 0 | 2010-01-01 | 0.000000 | 0.000000 |

| 1 | 2010-01-04 | 0.058362 | 0.058362 |

| 2 | 2010-01-05 | 0.001744 | 0.060106 |

| 3 | 2010-01-06 | 0.497980 | 0.558086 |

| 4 | 2010-01-07 | 0.061819 | 0.619905 |

Dividend Data Summary:

count 3913.000000

mean 0.186435

std 0.228265

min 0.000000

25% 0.022825

50% 0.095385

75% 0.271259

max 1.604820

Name: Daily_Div, dtype: float64

Days with zero dividends: 447 (11.4% of total)

Days with non-zero dividends: 3466 (88.6% of total)

Understanding Daily Dividends#

The build_daily_dividends() function extracts daily dividend information from the Bloomberg data and prepares it for use in the forward rate calculations.

Key observations:

The function extracts a specific column from a multi-index DataFrame

It converts dates, fills missing values with zeros, and sorts by date

Daily dividends are typically sparse - many days have zero dividends

The cumulative dividend is critical for the forward rate calculation

There may be seasonal patterns in dividend payments

The visualizations show both the daily dividend amounts (which are typically spiky) and the cumulative dividends (which grow over time). The monthly pattern chart helps identify any seasonality in dividend payments.

These dividend values will be used in the Div_Sum1 and Div_Sum2 calculations, which represent the expected dividends between the current date and the settlement dates.

def explore_barndorff_nielsen_filter():

"""

Demonstrate how the Barndorff-Nielsen outlier filter works with a synthetic dataset

"""

print("=== Exploring Barndorff-Nielsen Filter ===")

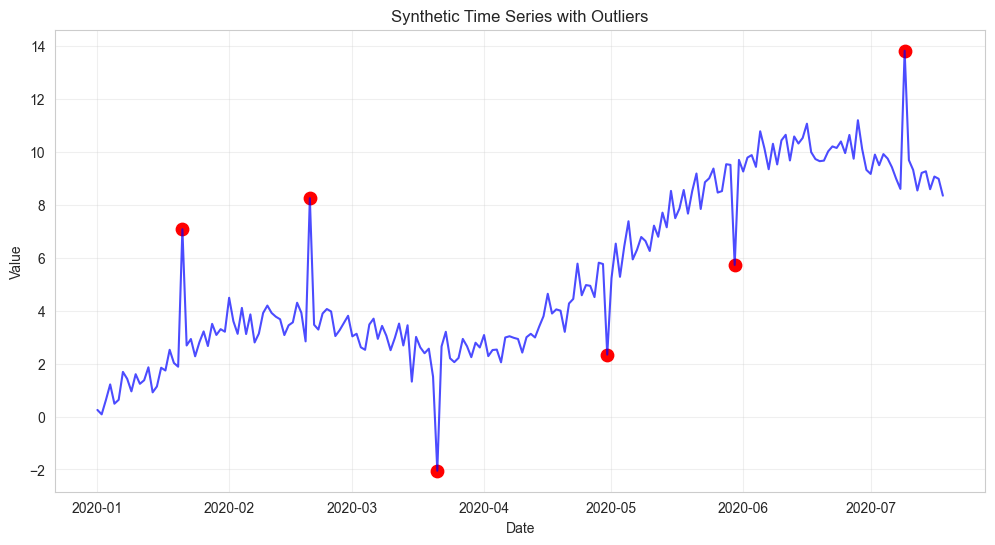

# Create a synthetic time series with some outliers

np.random.seed(42)

dates = pd.date_range(start='2020-01-01', periods=200)

# Base series with some seasonality and trend

base = np.linspace(0, 10, 200) + 2 * np.sin(np.linspace(0, 10, 200))

# Add noise

noise = np.random.normal(0, 0.5, 200)

# Add outliers

outliers_idx = [20, 50, 80, 120, 150, 190]

outliers = np.zeros(200)

for idx in outliers_idx:

outliers[idx] = np.random.choice([-1, 1]) * np.random.uniform(3, 5)

# Combined series

values = base + noise + outliers

# Create DataFrame

df = pd.DataFrame({

'Date': dates,

'value': values

})

# Visualize the original series

plt.figure(figsize=(12, 6))

plt.plot(df['Date'], df['value'], 'b-', alpha=0.7)

for idx in outliers_idx:

plt.scatter(df['Date'][idx], df['value'][idx], color='red', s=80)

plt.title('Synthetic Time Series with Outliers')

plt.xlabel('Date')

plt.ylabel('Value')

plt.grid(True, alpha=0.3)

plt.show()

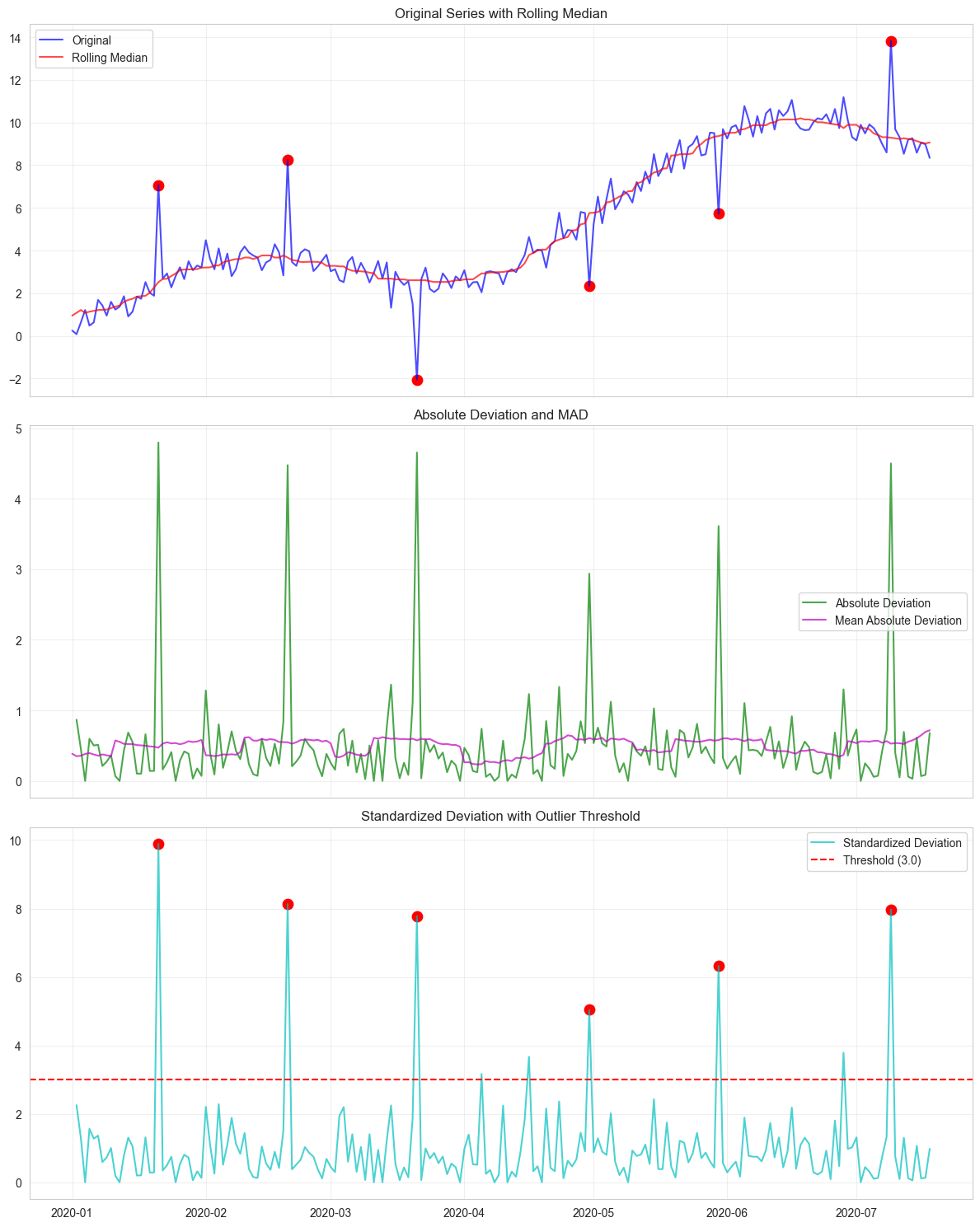

# Apply the Barndorff-Nielsen filter

window = 10 # Smaller window for demonstration

threshold = 3.0 # Lower threshold to catch all our synthetic outliers

# Sort the data

df = df.sort_values('Date')

# Calculate rolling median

rolling_median = df['value'].rolling(window=window*2+1, center=True, min_periods=1).median()

rolling_median_shifted = rolling_median.shift(1)

# Calculate absolute deviation

df['abs_dev'] = (df['value'] - rolling_median_shifted).abs()

# Calculate rolling MAD (Mean Absolute Deviation)

rolling_mad = df['abs_dev'].rolling(window=window*2+1, center=True, min_periods=1).mean()

rolling_mad_shifted = rolling_mad.shift(1)

# Calculate standardized deviation

df['std_dev'] = df['abs_dev'] / rolling_mad_shifted

# Determine outliers

df['is_outlier'] = df['std_dev'] >= threshold

df.loc[df['value'].isna(), 'is_outlier'] = False

# Create filtered series

df['value_filtered'] = df['value'].where(~df['is_outlier'], np.nan)

# Show step-by-step calculations for better understanding

print("\nStep-by-step filter process (showing sample rows):")

display(df[['Date', 'value', 'abs_dev', 'std_dev', 'is_outlier', 'value_filtered']].iloc[15:25])

# Visualize the filtering steps

fig, axes = plt.subplots(3, 1, figsize=(12, 15), sharex=True)

# Original with rolling median

axes[0].plot(df['Date'], df['value'], 'b-', alpha=0.7, label='Original')

axes[0].plot(df['Date'], rolling_median, 'r-', alpha=0.7, label='Rolling Median')

for idx in outliers_idx:

axes[0].scatter(df['Date'][idx], df['value'][idx], color='red', s=80)

axes[0].set_title('Original Series with Rolling Median')

axes[0].grid(True, alpha=0.3)

axes[0].legend()

# Absolute Deviation and Mean Absolute Deviation

axes[1].plot(df['Date'], df['abs_dev'], 'g-', alpha=0.7, label='Absolute Deviation')

axes[1].plot(df['Date'], rolling_mad, 'm-', alpha=0.7, label='Mean Absolute Deviation')

axes[1].set_title('Absolute Deviation and MAD')

axes[1].grid(True, alpha=0.3)

axes[1].legend()

# Standardized Deviation with Threshold

axes[2].plot(df['Date'], df['std_dev'], 'c-', alpha=0.7, label='Standardized Deviation')

axes[2].axhline(y=threshold, color='r', linestyle='--', label=f'Threshold ({threshold})')

for idx in outliers_idx:

if idx < len(df) and df['is_outlier'].iloc[idx]:

axes[2].scatter(df['Date'][idx], df['std_dev'][idx], color='red', s=80)

axes[2].set_title('Standardized Deviation with Outlier Threshold')

axes[2].grid(True, alpha=0.3)

axes[2].legend()

plt.tight_layout()

plt.show()

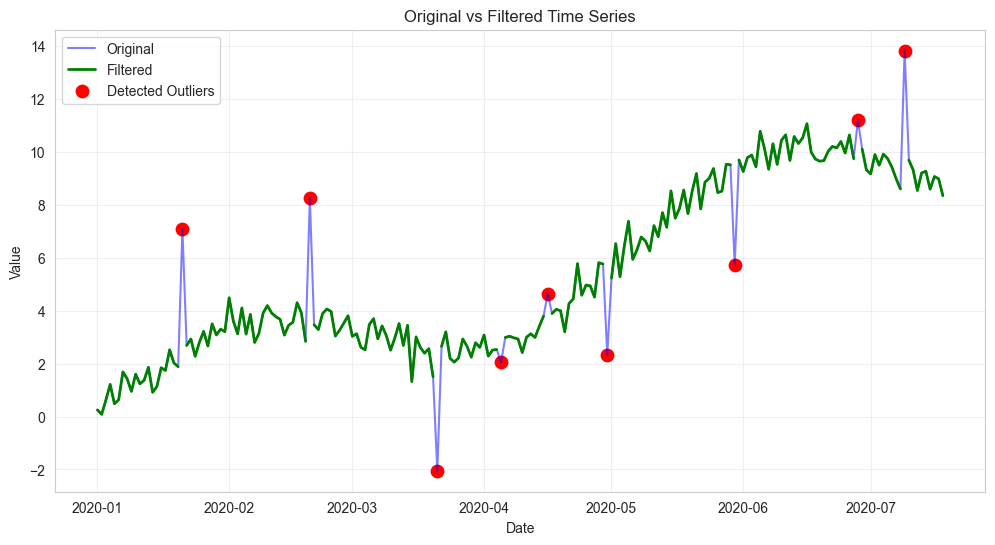

# Compare original vs filtered

plt.figure(figsize=(12, 6))

plt.plot(df['Date'], df['value'], 'b-', alpha=0.5, label='Original')

plt.plot(df['Date'], df['value_filtered'], 'g-', linewidth=2, label='Filtered')

detected_outliers = df[df['is_outlier']].index

plt.scatter(df['Date'][detected_outliers], df['value'][detected_outliers],

color='red', s=80, label='Detected Outliers')

plt.title('Original vs Filtered Time Series')

plt.xlabel('Date')

plt.ylabel('Value')

plt.grid(True, alpha=0.3)

plt.legend()

plt.show()

# Summary of outlier detection

detected_count = df['is_outlier'].sum()

print(f"\nSummary: Detected {detected_count} outliers out of {len(df)} observations")

# Check how many of our artificial outliers were detected

true_positive = 0

for idx in outliers_idx:

if idx < len(df) and df['is_outlier'].iloc[idx]:

true_positive += 1

print(f"True outliers detected: {true_positive} out of {len(outliers_idx)}")

if len(outliers_idx) > 0:

print(f"Detection rate: {true_positive/len(outliers_idx):.1%}")

return df

# Run the exploration

bn_filter_df = explore_barndorff_nielsen_filter()

=== Exploring Barndorff-Nielsen Filter ===

Step-by-step filter process (showing sample rows):

| Date | value | abs_dev | std_dev | is_outlier | value_filtered | |

|---|---|---|---|---|---|---|

| 15 | 2020-01-16 | 1.841408 | 0.103501 | 0.197860 | False | 1.841408 |

| 16 | 2020-01-17 | 1.737907 | 0.103501 | 0.203625 | False | 1.737907 |

| 17 | 2020-01-18 | 2.519580 | 0.661327 | 1.311529 | False | 2.519580 |

| 18 | 2020-01-19 | 2.022771 | 0.141783 | 0.284550 | False | 2.022771 |

| 19 | 2020-01-20 | 1.880988 | 0.141783 | 0.289496 | False | 1.880988 |

| 20 | 2020-01-21 | 7.071302 | 4.797679 | 9.889070 | True | NaN |

| 21 | 2020-01-22 | 2.682461 | 0.162881 | 0.345661 | False | 2.682461 |

| 22 | 2020-01-23 | 2.926694 | 0.265088 | 0.501126 | False | 2.926694 |

| 23 | 2020-01-24 | 2.273623 | 0.408838 | 0.746192 | False | 2.273623 |

| 24 | 2020-01-25 | 2.802253 | 0.000000 | 0.000000 | False | 2.802253 |

Summary: Detected 9 outliers out of 200 observations

True outliers detected: 6 out of 6

Detection rate: 100.0%

Understanding Barndorff-Nielsen Outlier Filter#

The Barndorff-Nielsen filter is a robust statistical method for detecting and removing outliers in time series data. Following the paper’s methedology:

Rolling Median Calculation:

For each point, calculate the median value within a window (±45 days by default)

This establishes a robust estimate of the “normal” value at each point

Absolute Deviation:

Calculate how far each value deviates from the rolling median

The shift(1) ensures we’re using previously known information

Mean Absolute Deviation (MAD):

Calculate the average of absolute deviations within the window

This establishes what constitutes a “normal” amount of deviation

Standardized Deviation:

Divide each absolute deviation by the MAD

This creates a standardized measure of how unusual each deviation is

Outlier Detection:

Points where standardized deviation ≥ threshold (default 10.0) are marked as outliers

These points are replaced with NaN in the filtered series

The filter is particularly useful for financial time series where sudden jumps can occur due to data errors or extreme market events that shouldn’t influence calculations of normal behavior.

In the spread calculation, this prevents outliers from distorting the implied forward rates.

def explore_forward_rate_calculation(index_code="SPX"):

"""

Explore the steps of the forward rate calculation visually

"""

print(f"=== Exploring Forward Rate Calculation for {index_code} ===")

# Load necessary data

fut_file = Path(PROCESSED_DIR) / f"{index_code}_Calendar_spread.csv"

ois_file = Path(PROCESSED_DIR) / "cleaned_ois_rates.csv"

# Check if files exist

if not fut_file.exists() or not ois_file.exists():

print("Required data files not found. Cannot proceed with exploration.")

return None

# Load calendar spreads

fut_df = pd.read_csv(fut_file)

fut_df["Date"] = pd.to_datetime(fut_df["Date"], errors="coerce")

fut_df.dropna(subset=["Date"], inplace=True)

fut_df["Term1_SettlementDate"] = pd.to_datetime(fut_df["Term1_SettlementDate"], errors="coerce")

fut_df["Term2_SettlementDate"] = pd.to_datetime(fut_df["Term2_SettlementDate"], errors="coerce")

fut_df.sort_values("Date", inplace=True)

# Display calendar spread data

print("\nFutures Calendar Spread data (first 5 rows):")

display(fut_df.head())

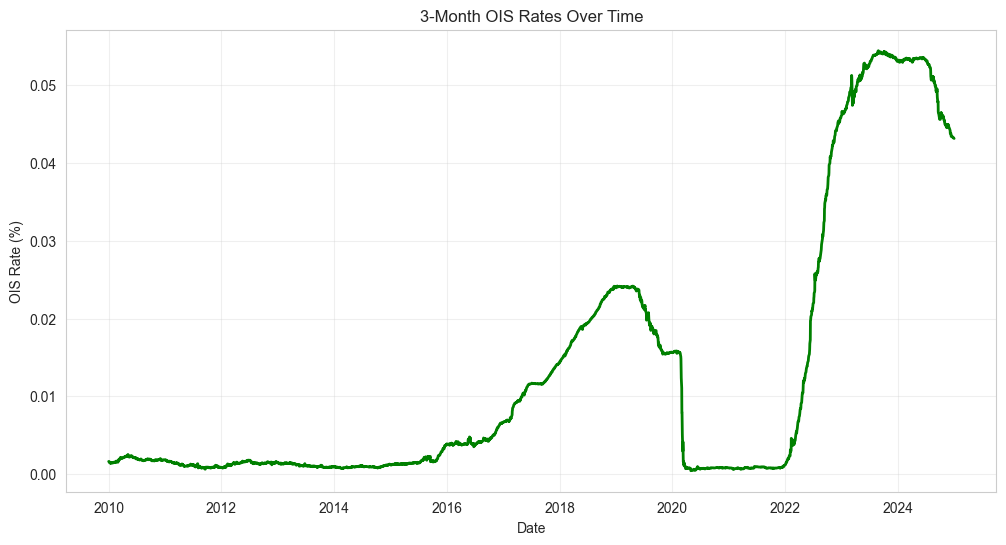

# Load OIS rates

ois_df = pd.read_csv(ois_file)

if "Date" not in ois_df.columns:

ois_df.rename(columns={"Unnamed: 0": "Date"}, inplace=True)

ois_df["Date"] = pd.to_datetime(ois_df["Date"], errors="coerce")

ois_df.sort_values("Date", inplace=True)

# Display OIS rates

print("\nOIS rates data (first 5 rows):")

display(ois_df.head())

# Chart the OIS rates

plt.figure(figsize=(12, 6))

plt.plot(ois_df["Date"], ois_df["OIS_3M"], 'g-', linewidth=2)

plt.title("3-Month OIS Rates Over Time")

plt.xlabel("Date")

plt.ylabel("OIS Rate (%)")

plt.grid(True, alpha=0.3)

plt.show()

# Merge futures and OIS data

merged_df = pd.merge_asof(

fut_df.sort_values("Date"),

ois_df,

on="Date",

direction="backward"

)

if "OIS_3M" in merged_df.columns:

merged_df.rename(columns={"OIS_3M": "OIS"}, inplace=True)

# Load dividends

div_df = build_daily_dividends(index_code)

div_df["CumDiv"] = div_df["Daily_Div"].cumsum()

# Merge with current date cumulative dividends

merged_df = pd.merge_asof(

merged_df.sort_values("Date"),

div_df[["Date", "CumDiv"]].sort_values("Date"),

on="Date",

direction="backward"

)

merged_df.rename(columns={"CumDiv": "CumDiv_current"}, inplace=True)

# Merge with Term1 and Term2 settlement date cumulative dividends

t1_df = div_df.rename(columns={"Date": "Term1_SettlementDate", "CumDiv": "CumDiv_Term1"})

merged_df = pd.merge_asof(

merged_df.sort_values("Term1_SettlementDate"),

t1_df.sort_values("Term1_SettlementDate"),

on="Term1_SettlementDate",

direction="backward"

)

t2_df = div_df.rename(columns={"Date": "Term2_SettlementDate", "CumDiv": "CumDiv_Term2"})

merged_df = pd.merge_asof(

merged_df.sort_values("Term2_SettlementDate"),

t2_df.sort_values("Term2_SettlementDate"),

on="Term2_SettlementDate",

direction="backward"

)

# Calculate dividend sums

merged_df["Div_Sum1"] = merged_df["CumDiv_Term1"] - merged_df["CumDiv_current"]

merged_df["Div_Sum2"] = merged_df["CumDiv_Term2"] - merged_df["CumDiv_current"]

# Display intermediate calculation

print("\nIntermediate calculation with dividend sums (sample rows):")

display(merged_df[["Date", "Term1_TTM", "Term2_TTM", "Term1_Futures_Price",

"Term2_Futures_Price", "OIS", "Div_Sum1", "Div_Sum2"]].head())

# Remove rows with missing TTM or price data

merged_df.dropna(subset=["Term1_TTM", "Term2_TTM", "Term1_Futures_Price", "Term2_Futures_Price"], inplace=True)

# Step-by-step calculation visualization

# 1. Compounding dividends

merged_df["Div_Sum1_Comp"] = merged_df["Div_Sum1"] * (

((merged_df["Term1_TTM"] / 2.0) / 360.0) * merged_df["OIS"] + 1.0

)

merged_df["Div_Sum2_Comp"] = merged_df["Div_Sum2"] * (

((merged_df["Term2_TTM"] / 2.0) / 360.0) * merged_df["OIS"] + 1.0

)

# Show effect of compounding

print("\nEffect of compounding on dividends (sample rows):")

display(merged_df[["Date", "Div_Sum1", "Div_Sum1_Comp", "Div_Sum2", "Div_Sum2_Comp"]].head())

# 2. Implied forward rate calculation

merged_df["implied_forward_raw"] = (

(merged_df["Term2_Futures_Price"] + merged_df["Div_Sum2_Comp"]) /

(merged_df["Term1_Futures_Price"] + merged_df["Div_Sum1_Comp"])

- 1.0

)

dt = merged_df["Term2_TTM"] - merged_df["Term1_TTM"]

merged_df[f"cal_{index_code}_rf"] = np.where(

dt > 0,

100.0 * merged_df["implied_forward_raw"] * (360.0 / dt),

np.nan

)

# 3. OIS-implied forward rate

merged_df["ois_fwd_raw"] = (

(1.0 + merged_df["OIS"] * merged_df["Term2_TTM"] / 360.0) /

(1.0 + merged_df["OIS"] * merged_df["Term1_TTM"] / 360.0)

- 1.0

)

merged_df[f"ois_fwd_{index_code}"] = np.where(

dt > 0,

merged_df["ois_fwd_raw"] * (360.0 / dt) * 100.0,

np.nan

)

# 4. Spread calculation

spread_col = f"spread_{index_code}"

merged_df[spread_col] = merged_df[f"cal_{index_code}_rf"] - merged_df[f"ois_fwd_{index_code}"]

# Show forward rate calculations

print("\nForward rate calculations (sample rows):")

display(merged_df[[

"Date",

"implied_forward_raw",

f"cal_{index_code}_rf",

"ois_fwd_raw",

f"ois_fwd_{index_code}",

spread_col

]].head())

# Apply Barndorff-Nielsen filter

filtered_df = barndorff_nielsen_filter(merged_df, spread_col, date_col="Date", window=45, threshold=10)

# Set outliers to NaN

out_mask = filtered_df[f"{spread_col}_filtered"].isna()

filtered_df.loc[out_mask, f"cal_{index_code}_rf"] = np.nan

filtered_df.loc[out_mask, spread_col] = np.nan

# Multiply spread by 100 for bps

filtered_df[spread_col] = filtered_df[spread_col] * 100.0

# Set index to Date for time series plots

filtered_df.set_index("Date", inplace=True)

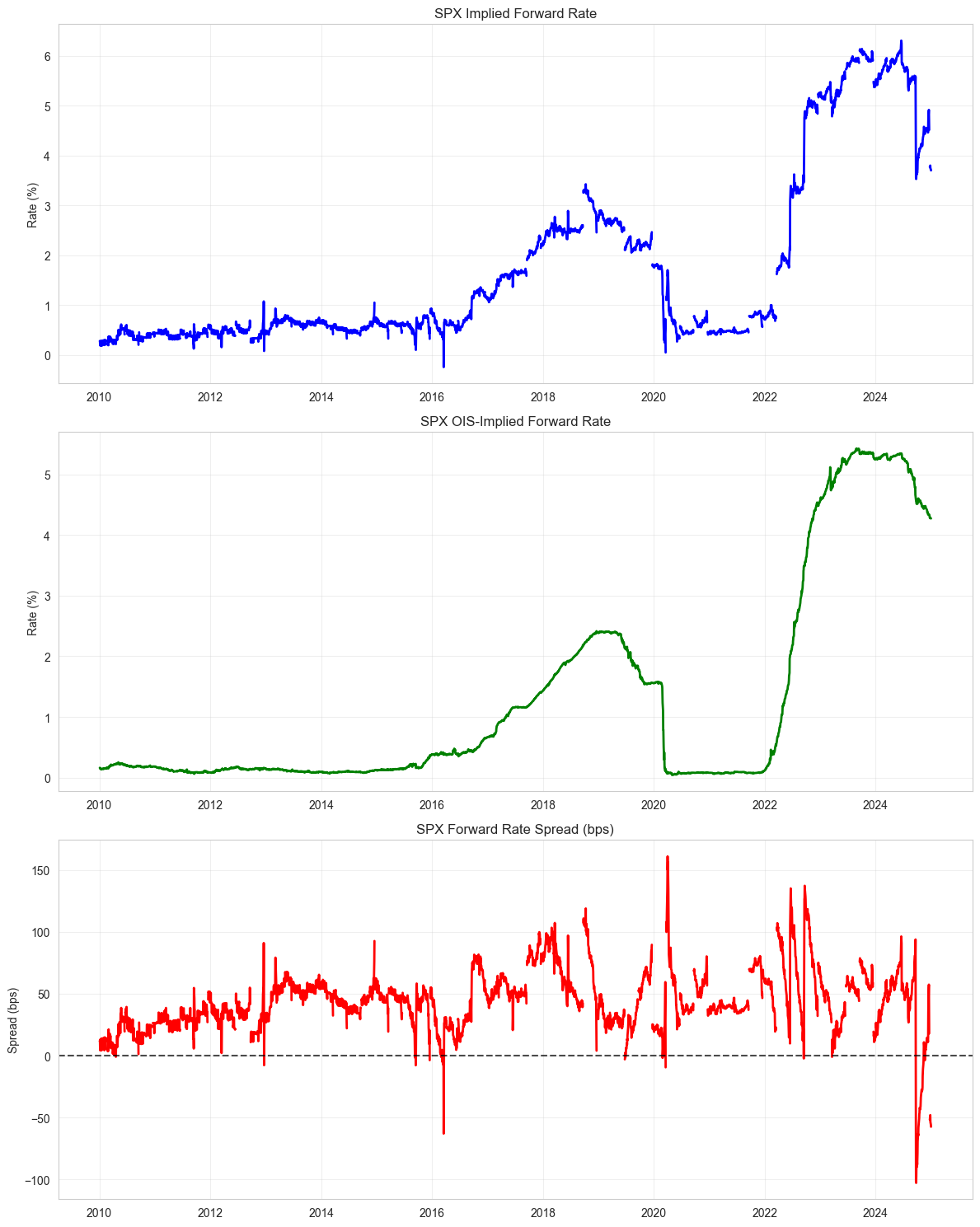

# Visualize the forward rates and spread

plt.figure(figsize=(12, 15))

# Plot 1: Implied Forward Rate

plt.subplot(3, 1, 1)

plt.plot(filtered_df.index, filtered_df[f"cal_{index_code}_rf"], 'b-', linewidth=2)

plt.title(f"{index_code} Implied Forward Rate")

plt.ylabel("Rate (%)")

plt.grid(True, alpha=0.3)

# Plot 2: OIS Forward Rate

plt.subplot(3, 1, 2)

plt.plot(filtered_df.index, filtered_df[f"ois_fwd_{index_code}"], 'g-', linewidth=2)

plt.title(f"{index_code} OIS-Implied Forward Rate")

plt.ylabel("Rate (%)")

plt.grid(True, alpha=0.3)

# Plot 3: Spread

plt.subplot(3, 1, 3)

plt.plot(filtered_df.index, filtered_df[spread_col], 'r-', linewidth=2)

plt.axhline(y=0, color='k', linestyle='--', alpha=0.7)

plt.title(f"{index_code} Forward Rate Spread (bps)")

plt.ylabel("Spread (bps)")

plt.grid(True, alpha=0.3)

plt.tight_layout()

plt.show()

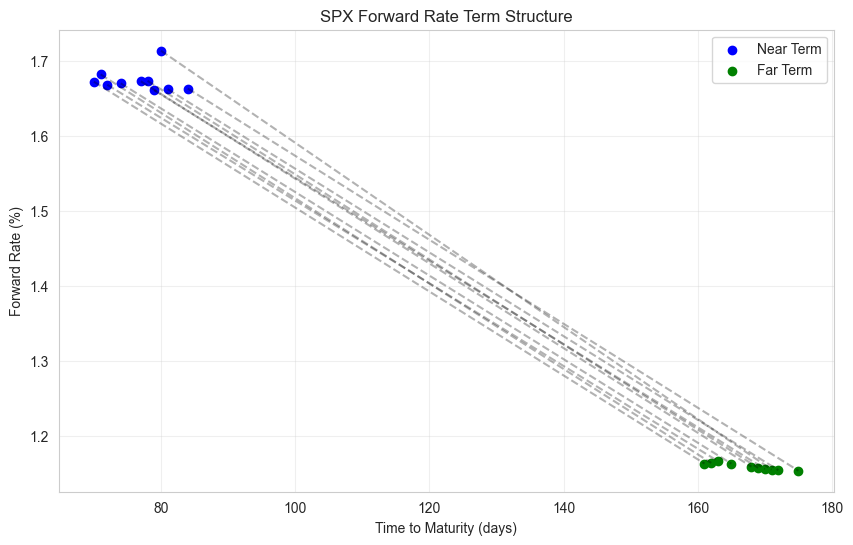

# Visualize the term structure

plt.figure(figsize=(10, 6))

# Get a sample date for demonstration

sample_date = filtered_df.index[len(filtered_df) // 2] # Middle of the dataset

print(f"\nTerm structure visualization for date: {sample_date}")

# Filter for a reasonable window around the sample date

date_window = 5 # Days

sample_window = filtered_df.index.get_indexer([sample_date], method='nearest')[0]

sample_window_start = max(0, sample_window - date_window)

sample_window_end = min(len(filtered_df), sample_window + date_window)

sample_data = filtered_df.iloc[sample_window_start:sample_window_end]

# Plot term structure

for date in sample_data.index:

row = filtered_df.loc[date]

plt.scatter(row["Term1_TTM"], row[f"cal_{index_code}_rf"], color='blue', label='Near Term' if date == sample_data.index[0] else "")

plt.scatter(row["Term2_TTM"], row[f"ois_fwd_{index_code}"], color='green', label='Far Term' if date == sample_data.index[0] else "")

# Connect the points with a line

plt.plot([row["Term1_TTM"], row["Term2_TTM"]],

[row[f"cal_{index_code}_rf"], row[f"ois_fwd_{index_code}"]],

'k--', alpha=0.3)

plt.title(f"{index_code} Forward Rate Term Structure")

plt.xlabel("Time to Maturity (days)")

plt.ylabel("Forward Rate (%)")

plt.grid(True, alpha=0.3)

plt.legend()

plt.show()

return filtered_df

# Run the exploration

forward_rate_df = explore_forward_rate_calculation("SPX")

=== Exploring Forward Rate Calculation for SPX ===

Futures Calendar Spread data (first 5 rows):

| Date | Term1_Futures_Price | Term1_Volume | Term1_OpenInterest | Term1_ContractSpec | Term1_SettlementDate | Term1_TTM | Term2_Futures_Price | Term2_Volume | Term2_OpenInterest | Term2_ContractSpec | Term2_SettlementDate | Term2_TTM | Index | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-04 | 1128.75 | 1282633.0 | 2440458.0 | MAR 10 | 2010-03-19 | 74.0 | 1124.00 | 1641.0 | 3354.0 | JUN 10 | 2010-06-18 | 165.0 | SPX |

| 1 | 2010-01-05 | 1132.25 | 1368386.0 | 2402850.0 | MAR 10 | 2010-03-19 | 73.0 | 1127.50 | 686.0 | 3432.0 | JUN 10 | 2010-06-18 | 164.0 | SPX |

| 2 | 2010-01-06 | 1133.00 | 1252015.0 | 2396493.0 | MAR 10 | 2010-03-19 | 72.0 | 1128.00 | 1163.0 | 3713.0 | JUN 10 | 2010-06-18 | 163.0 | SPX |

| 3 | 2010-01-07 | 1137.50 | 1553963.0 | 2406352.0 | MAR 10 | 2010-03-19 | 71.0 | 1132.50 | 1135.0 | 4154.0 | JUN 10 | 2010-06-18 | 162.0 | SPX |

| 4 | 2010-01-08 | 1141.50 | 1508175.0 | 2758348.0 | MAR 10 | 2010-03-19 | 70.0 | 1136.75 | 1080.0 | 17466.0 | JUN 10 | 2010-06-18 | 161.0 | SPX |

OIS rates data (first 5 rows):

| Date | OIS_3M | |

|---|---|---|

| 0 | 2010-01-01 | 0.00162 |

| 1 | 2010-01-04 | 0.00162 |

| 2 | 2010-01-05 | 0.00155 |

| 3 | 2010-01-06 | 0.00146 |

| 4 | 2010-01-07 | 0.00145 |

[SPX] Building daily dividend table

Primary input file not found, switching to cached data

[SPX] daily dividends final shape: (3913, 2)

[SPX] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.058362

2 2010-01-05 0.001744

3 2010-01-06 0.497980

4 2010-01-07 0.061819

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.113508

9 2010-01-14 0.021957

Intermediate calculation with dividend sums (sample rows):

| Date | Term1_TTM | Term2_TTM | Term1_Futures_Price | Term2_Futures_Price | OIS | Div_Sum1 | Div_Sum2 | |

|---|---|---|---|---|---|---|---|---|

| 0 | 2010-01-04 | 74.0 | 165.0 | 1128.75 | 1124.00 | 0.00162 | 4.840390 | 10.382986 |

| 1 | 2010-01-05 | 73.0 | 164.0 | 1132.25 | 1127.50 | 0.00155 | 4.838646 | 10.381242 |

| 2 | 2010-01-06 | 72.0 | 163.0 | 1133.00 | 1128.00 | 0.00146 | 4.340666 | 9.883262 |

| 3 | 2010-01-07 | 71.0 | 162.0 | 1137.50 | 1132.50 | 0.00145 | 4.278847 | 9.821443 |

| 4 | 2010-01-08 | 70.0 | 161.0 | 1141.50 | 1136.75 | 0.00143 | 4.278847 | 9.821443 |

Effect of compounding on dividends (sample rows):

| Date | Div_Sum1 | Div_Sum1_Comp | Div_Sum2 | Div_Sum2_Comp | |

|---|---|---|---|---|---|

| 0 | 2010-01-04 | 4.840390 | 4.841196 | 10.382986 | 10.386841 |

| 1 | 2010-01-05 | 4.838646 | 4.839406 | 10.381242 | 10.384907 |

| 2 | 2010-01-06 | 4.340666 | 4.341300 | 9.883262 | 9.886529 |

| 3 | 2010-01-07 | 4.278847 | 4.279459 | 9.821443 | 9.824647 |

| 4 | 2010-01-08 | 4.278847 | 4.279442 | 9.821443 | 9.824584 |

Forward rate calculations (sample rows):

| Date | implied_forward_raw | cal_SPX_rf | ois_fwd_raw | ois_fwd_SPX | spread_SPX | |

|---|---|---|---|---|---|---|

| 0 | 2010-01-04 | 0.000702 | 0.277667 | 0.000409 | 0.161946 | 0.115721 |

| 1 | 2010-01-05 | 0.000700 | 0.276762 | 0.000392 | 0.154951 | 0.121811 |

| 2 | 2010-01-06 | 0.000479 | 0.189648 | 0.000369 | 0.145957 | 0.043691 |

| 3 | 2010-01-07 | 0.000477 | 0.188897 | 0.000366 | 0.144959 | 0.043939 |

| 4 | 2010-01-08 | 0.000694 | 0.274539 | 0.000361 | 0.142960 | 0.131579 |

Barndorff-Nielsen filter: flagged 47 outliers in spread_SPX

Term structure visualization for date: 2017-06-30 00:00:00

Understanding the Forward Rate Calculation Process#

When computing equity spot-futures arbitrage for an index ( S_t ) paying dividends from ( t ) to ( t + \tau ), we combine:

Futures Prices (from the nearest and next-nearest futures contracts)

OIS Rates (as a proxy for the risk-free rate)

Realized Dividends (as a simple forecast of expected dividends)

These are merged into a single DataFrame, from which we derive an implied forward rate ( \cal{rf} ) and compare it with the OIS-implied forward rate to compute an arbitrage spread.

1. Data Preparation & Merging#

Calendar Spread Data

Provides columns for:Term1_Futures_PriceandTerm2_Futures_Price(prices for near-term and deferred futures)Term1_SettlementDateandTerm2_SettlementDateTerm1_TTMandTerm2_TTM(time-to-maturity in days)

OIS Rates

Contains daily 3-month OIS rates, merged into the calendar spread data via an as-of backward merge onDate.Dividends

We accumulate daily dividends into a

CumDivseries.Merged at both the current date and each futures settlement date to approximate how much dividend would be paid between now and each maturity.

2. Dividend Sums#

Let:

\( \text{CumDiv}_\text{current} \) = cumulative dividend at the current date

\( \text{CumDiv}_{\text{Term1}} \) = cumulative dividend at the Term1 settlement date

\( \text{CumDiv}_{\text{Term2}} \) = cumulative dividend at the Term2 settlement date

Then:

3. Dividend Compounding#

We apply a half-interval compounding for each dividend sum:

4. Implied Forward Rate#

From Hazelkorn et al. (2021), the raw implied forward rate (over (\tau_1) to (\tau_2)) is:

We annualize this raw rate by multiplying according to the difference in time-to-maturity ((\text{Term2_TTM} - \text{Term1_TTM})):

5. OIS-Implied Forward Rate#

Similarly, we estimate how OIS would imply a forward rate between (\tau_1) and (\tau_2):

We annualize it in the same manner:

6. Spread Calculation#

We define the arbitrage spread in basis points (bps) as:

A positive spread indicates the futures-implied forward rate is higher than the OIS-implied rate.

7. Outlier Filtering#

We apply a Barndorff–Nielsen filter on spread_{index} to flag outliers based on rolling median absolute deviation. These flagged values are set to NaN to remove spurious spikes or data errors.

Interpretation

Spot-Futures Parity would suggest the forward rate extracted from futures = OIS rate, making the spread near zero.

A non-zero spread implies potential frictions, funding constraints, or margin requirements that might limit arbitrage.

Futures + Dividends yield an equity-implied forward rate over (\tau_1 \to \tau_2).

OIS gives an alternative “risk-free” benchmark.

Comparing them highlights possible arbitrage or funding market dislocations.

# 4. Comparing Forward Rates Across Indices

def explore_cross_index_comparison():

"""

Compare forward rates and spreads across different indices to identify patterns and relationships

"""

print("=== Exploring Cross-Index Forward Rate Analysis ===")

# Process data for all indices

results = {}

for idx in INDEX_CODES:

print(f"\nProcessing {idx}...")

fut_file = Path(PROCESSED_DIR) / f"{idx}_Calendar_spread.csv"

if not fut_file.exists():

print(f" Missing futures file for {idx}, skipping.")

continue

# Run the forward rate calculation

df_res = process_index_forward_rates(idx)

if df_res is not None and not df_res.empty:

results[idx] = df_res

if not results:

print("No valid results to compare. Ending exploration.")

return None

# Create a unified DataFrame with spreads from all indices

# First, find the union of all dates

all_dates = set()

for idx, df in results.items():

all_dates.update(df.index.tolist())

# Sort dates

date_index = pd.to_datetime(sorted(all_dates))

# Create a DataFrame with all spreads

spreads_df = pd.DataFrame(index=date_index)

for idx, df in results.items():

spread_col = f"spread_{idx}"

# Forward fill to handle missing dates

spreads_df[spread_col] = df[spread_col].reindex(date_index).ffill()

# Show the head of the combined spreads

print("\nCombined spreads data (first rows):")

display(spreads_df.head())

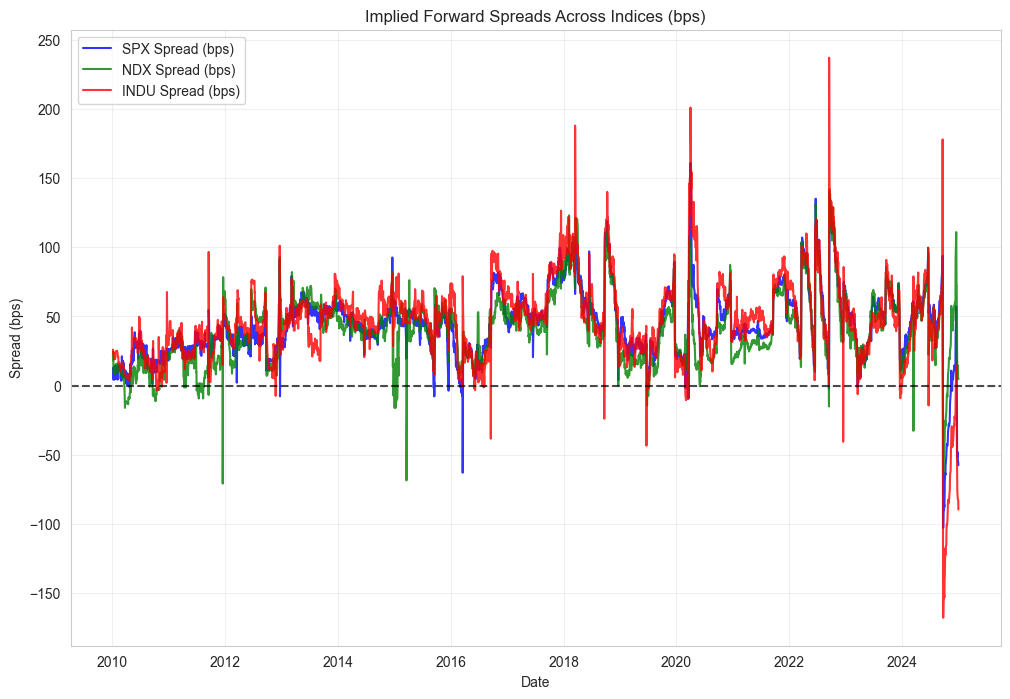

# Visualize combined spreads

plt.figure(figsize=(12, 8))

colors = {"SPX": "blue", "NDX": "green", "INDU": "red"}

for idx in results.keys():

spread_col = f"spread_{idx}"

plt.plot(

spreads_df.index,

spreads_df[spread_col],

color=colors.get(idx, "black"),

alpha=0.8,

label=f"{idx} Spread (bps)"

)

plt.axhline(0, color="k", linestyle="--", alpha=0.7)

plt.title("Implied Forward Spreads Across Indices (bps)")

plt.xlabel("Date")

plt.ylabel("Spread (bps)")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

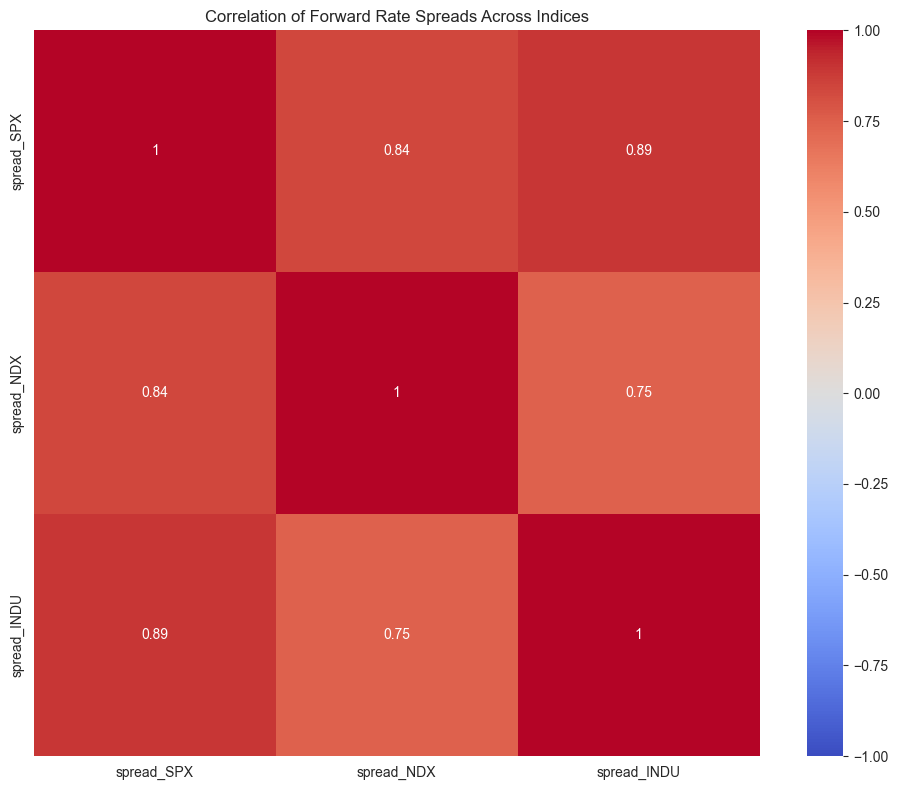

# Calculate correlations between spreads

if len(results) > 1:

corr_matrix = spreads_df.corr()

print("\nCorrelation matrix of spreads:")

display(corr_matrix)

# Visualize correlations

plt.figure(figsize=(10, 8))

sns.heatmap(corr_matrix, annot=True, cmap='coolwarm', vmin=-1, vmax=1, square=True)

plt.title("Correlation of Forward Rate Spreads Across Indices")

plt.tight_layout()

plt.show()

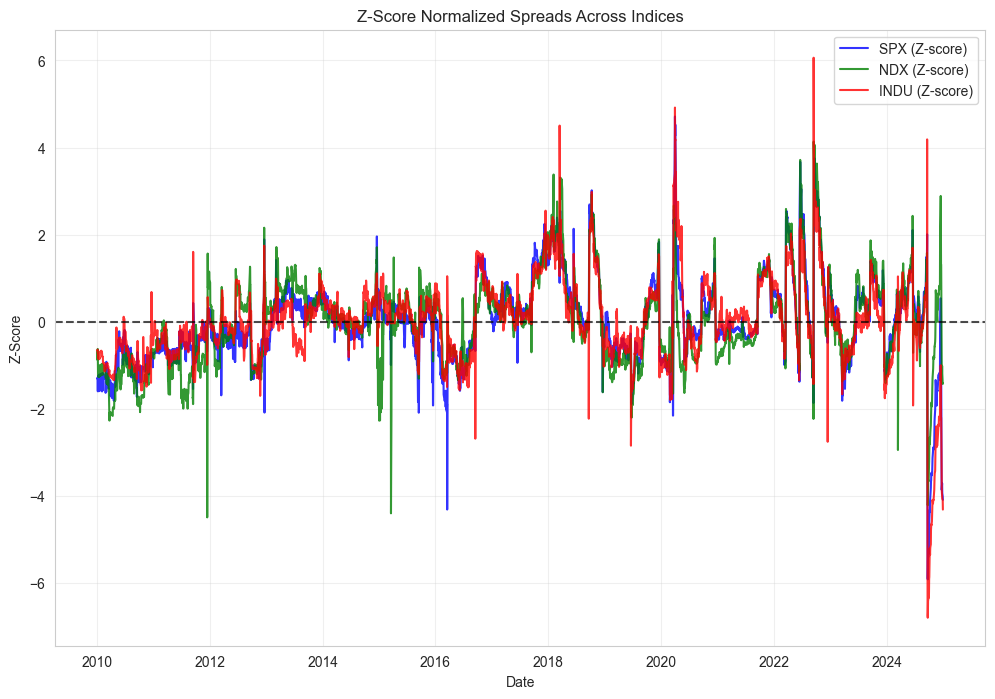

# Z-score normalized spreads for comparison

if not spreads_df.empty:

# Calculate z-scores for each spread

z_scores_df = pd.DataFrame(index=spreads_df.index)

for col in spreads_df.columns:

z_scores_df[col] = (spreads_df[col] - spreads_df[col].mean()) / spreads_df[col].std()

# Visualize normalized spreads

plt.figure(figsize=(12, 8))

for idx in results.keys():

spread_col = f"spread_{idx}"

plt.plot(

z_scores_df.index,

z_scores_df[spread_col],

color=colors.get(idx, "black"),

alpha=0.8,

label=f"{idx} (Z-score)"

)

plt.axhline(0, color="k", linestyle="--", alpha=0.7)

plt.title("Z-Score Normalized Spreads Across Indices")

plt.xlabel("Date")

plt.ylabel("Z-Score")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

return spreads_df

cross_index_df = explore_cross_index_comparison()

=== Exploring Cross-Index Forward Rate Analysis ===

Processing SPX...

[SPX] Starting forward rate computation

[SPX] Loaded futures shape: (3781, 14)

[SPX] Dropped 0 rows lacking a valid Date in futures.

[SPX] as-of merged OIS: from 3781 -> 3781 rows (should be same).

[SPX] Building daily dividend table

Primary input file not found, switching to cached data

[SPX] daily dividends final shape: (3913, 2)

[SPX] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.058362

2 2010-01-05 0.001744

3 2010-01-06 0.497980

4 2010-01-07 0.061819

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.113508

9 2010-01-14 0.021957

[SPX] as-of merged CumDiv at current date: from 3781 -> 3781 rows.

[SPX] Sample merged rows with cumulative div:

Date Term1_Futures_Price Term1_Volume Term1_OpenInterest \

0 2010-01-04 1128.75 1282633.0 2440458.0

1 2010-01-05 1132.25 1368386.0 2402850.0

2 2010-01-06 1133.00 1252015.0 2396493.0

3 2010-01-07 1137.50 1553963.0 2406352.0

4 2010-01-08 1141.50 1508175.0 2758348.0

5 2010-01-11 1142.50 1444997.0 2427453.0

6 2010-01-12 1134.00 2089364.0 2439036.0

7 2010-01-13 1141.50 2110033.0 2475322.0

8 2010-01-14 1145.25 1346436.0 2473392.0

9 2010-01-15 1132.25 2031715.0 2454453.0

Term1_ContractSpec Term1_SettlementDate Term1_TTM Term2_Futures_Price \

0 MAR 10 2010-03-19 74.0 1124.00

1 MAR 10 2010-03-19 73.0 1127.50

2 MAR 10 2010-03-19 72.0 1128.00

3 MAR 10 2010-03-19 71.0 1132.50

4 MAR 10 2010-03-19 70.0 1136.75

5 MAR 10 2010-03-19 67.0 1137.50

6 MAR 10 2010-03-19 66.0 1129.00

7 MAR 10 2010-03-19 65.0 1136.75

8 MAR 10 2010-03-19 64.0 1140.25

9 MAR 10 2010-03-19 63.0 1127.50

Term2_Volume Term2_OpenInterest Term2_ContractSpec Term2_SettlementDate \

0 1641.0 3354.0 JUN 10 2010-06-18

1 686.0 3432.0 JUN 10 2010-06-18

2 1163.0 3713.0 JUN 10 2010-06-18

3 1135.0 4154.0 JUN 10 2010-06-18

4 1080.0 17466.0 JUN 10 2010-06-18

5 419.0 4638.0 JUN 10 2010-06-18

6 481.0 4765.0 JUN 10 2010-06-18

7 1174.0 5389.0 JUN 10 2010-06-18

8 333.0 5357.0 JUN 10 2010-06-18

9 1432.0 5936.0 JUN 10 2010-06-18

Term2_TTM Index OIS CumDiv_current

0 165.0 SPX 0.001620 0.058362

1 164.0 SPX 0.001550 0.060106

2 163.0 SPX 0.001460 0.558086

3 162.0 SPX 0.001450 0.619905

4 161.0 SPX 0.001430 0.619905

5 158.0 SPX 0.001430 0.619905

6 157.0 SPX 0.001415 0.619905

7 156.0 SPX 0.001470 0.733413

8 155.0 SPX 0.001430 0.755370

9 154.0 SPX 0.001380 0.799620

[SPX] as-of merged CumDiv for Term1: from 3781 -> 3781 rows.

[SPX] as-of merged CumDiv for Term2: from 3781 -> 3781 rows.

[SPX] Dropped 0 rows missing TTM or Futures_Price.

Barndorff-Nielsen filter: flagged 47 outliers in spread_SPX

[SPX] Setting 47 outliers to NaN for cal_SPX_rf & spread_SPX

[SPX] Final forward rates shape: (3781, 29)

[SPX] Sample final rows:

cal_SPX_rf ois_fwd_SPX spread_SPX

Date

2024-12-24 3.778583 4.287412 -50.882869

2024-12-26 3.796641 4.277498 -48.085749

2024-12-27 3.741256 4.277624 -53.636841

2024-12-30 3.717731 4.275913 -55.818186

2024-12-31 3.698950 4.274017 -57.506667

Processing NDX...

[NDX] Starting forward rate computation

[NDX] Loaded futures shape: (3781, 14)

[NDX] Dropped 0 rows lacking a valid Date in futures.

[NDX] as-of merged OIS: from 3781 -> 3781 rows (should be same).

[NDX] Building daily dividend table

Primary input file not found, switching to cached data

[NDX] daily dividends final shape: (3913, 2)

[NDX] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.148515

2 2010-01-05 0.000000

3 2010-01-06 0.000000

4 2010-01-07 0.000000

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.000000

9 2010-01-14 0.113752

[NDX] as-of merged CumDiv at current date: from 3781 -> 3781 rows.

[NDX] Sample merged rows with cumulative div:

Date Term1_Futures_Price Term1_Volume Term1_OpenInterest \

0 2010-01-04 1886.75 204140.0 314877.0

1 2010-01-05 1885.25 207245.0 309080.0

2 2010-01-06 1878.50 259627.0 310532.0

3 2010-01-07 1877.50 239907.0 317226.0

4 2010-01-08 1890.00 267314.0 379994.0

5 2010-01-11 1883.50 243454.0 314557.0

6 2010-01-12 1865.50 326600.0 306114.0

7 2010-01-13 1882.50 312998.0 331168.0

8 2010-01-14 1888.25 204465.0 324274.0

9 2010-01-15 1862.25 343007.0 320266.0

Term1_ContractSpec Term1_SettlementDate Term1_TTM Term2_Futures_Price \

0 MAR 10 2010-03-19 74.0 1884.75

1 MAR 10 2010-03-19 73.0 1883.00

2 MAR 10 2010-03-19 72.0 1876.50

3 MAR 10 2010-03-19 71.0 1875.00

4 MAR 10 2010-03-19 70.0 1887.25

5 MAR 10 2010-03-19 67.0 1880.75

6 MAR 10 2010-03-19 66.0 1862.75

7 MAR 10 2010-03-19 65.0 1879.75

8 MAR 10 2010-03-19 64.0 1885.50

9 MAR 10 2010-03-19 63.0 1859.75

Term2_Volume Term2_OpenInterest Term2_ContractSpec Term2_SettlementDate \

0 33.0 671.0 JUN 10 2010-06-18

1 74.0 651.0 JUN 10 2010-06-18

2 33.0 665.0 JUN 10 2010-06-18

3 47.0 672.0 JUN 10 2010-06-18

4 1001.0 6163.0 JUN 10 2010-06-18

5 288.0 898.0 JUN 10 2010-06-18

6 311.0 1077.0 JUN 10 2010-06-18

7 710.0 1699.0 JUN 10 2010-06-18

8 784.0 2401.0 JUN 10 2010-06-18

9 272.0 2533.0 JUN 10 2010-06-18

Term2_TTM Index OIS CumDiv_current

0 165.0 NDX 0.001620 0.148515

1 164.0 NDX 0.001550 0.148515

2 163.0 NDX 0.001460 0.148515

3 162.0 NDX 0.001450 0.148515

4 161.0 NDX 0.001430 0.148515

5 158.0 NDX 0.001430 0.148515

6 157.0 NDX 0.001415 0.148515

7 156.0 NDX 0.001470 0.148515

8 155.0 NDX 0.001430 0.262267

9 154.0 NDX 0.001380 0.262267

[NDX] as-of merged CumDiv for Term1: from 3781 -> 3781 rows.

[NDX] as-of merged CumDiv for Term2: from 3781 -> 3781 rows.

[NDX] Dropped 0 rows missing TTM or Futures_Price.

Barndorff-Nielsen filter: flagged 48 outliers in spread_NDX

[NDX] Setting 48 outliers to NaN for cal_NDX_rf & spread_NDX

[NDX] Final forward rates shape: (3781, 29)

[NDX] Sample final rows:

cal_NDX_rf ois_fwd_NDX spread_NDX

Date

2024-12-24 4.341428 4.287412 5.401572

2024-12-26 4.426357 4.277498 14.885916

2024-12-27 4.384662 4.277624 10.703781

2024-12-30 4.322400 4.275913 4.648708

2024-12-31 4.323851 4.274017 4.983391

Processing INDU...

[INDU] Starting forward rate computation

[INDU] Loaded futures shape: (3780, 14)

[INDU] Dropped 0 rows lacking a valid Date in futures.

[INDU] as-of merged OIS: from 3780 -> 3780 rows (should be same).

[INDU] Building daily dividend table

Primary input file not found, switching to cached data

[INDU] daily dividends final shape: (3913, 2)

[INDU] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.377875

2 2010-01-05 0.000000

3 2010-01-06 6.763957

4 2010-01-07 1.360349

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.000000

9 2010-01-14 0.000000

[INDU] as-of merged CumDiv at current date: from 3780 -> 3780 rows.

[INDU] Sample merged rows with cumulative div:

Date Term1_Futures_Price Term1_Volume Term1_OpenInterest \

0 2010-01-04 10519.0 93770.0 69420.0

1 2010-01-05 10515.0 93287.0 65749.0

2 2010-01-06 10516.0 97172.0 63888.0

3 2010-01-07 10545.0 112280.0 67401.0

4 2010-01-08 10566.0 79925.0 61714.0

5 2010-01-11 10604.0 93891.0 63318.0

6 2010-01-12 10588.0 126885.0 62710.0

7 2010-01-13 10628.0 113576.0 63479.0

8 2010-01-14 10663.0 80520.0 64500.0

9 2010-01-15 10563.0 140591.0 66826.0

Term1_ContractSpec Term1_SettlementDate Term1_TTM Term2_Futures_Price \

0 MAR 10 2010-03-19 74.0 10459.0

1 MAR 10 2010-03-19 73.0 10455.0

2 MAR 10 2010-03-19 72.0 10455.0

3 MAR 10 2010-03-19 71.0 10484.0

4 MAR 10 2010-03-19 70.0 10505.0

5 MAR 10 2010-03-19 67.0 10542.0

6 MAR 10 2010-03-19 66.0 10527.0

7 MAR 10 2010-03-19 65.0 10566.0

8 MAR 10 2010-03-19 64.0 10601.0

9 MAR 10 2010-03-19 63.0 10501.0

Term2_Volume Term2_OpenInterest Term2_ContractSpec Term2_SettlementDate \

0 100.0 175.0 JUN 10 2010-06-18

1 26.0 173.0 JUN 10 2010-06-18

2 157.0 193.0 JUN 10 2010-06-18

3 34.0 180.0 JUN 10 2010-06-18

4 146.0 531.0 JUN 10 2010-06-18

5 45.0 230.0 JUN 10 2010-06-18

6 55.0 234.0 JUN 10 2010-06-18

7 21.0 208.0 JUN 10 2010-06-18

8 11.0 206.0 JUN 10 2010-06-18

9 80.0 221.0 JUN 10 2010-06-18

Term2_TTM Index OIS CumDiv_current

0 165.0 INDU 0.001620 0.377875

1 164.0 INDU 0.001550 0.377875

2 163.0 INDU 0.001460 7.141832

3 162.0 INDU 0.001450 8.502181

4 161.0 INDU 0.001430 8.502181

5 158.0 INDU 0.001430 8.502181

6 157.0 INDU 0.001415 8.502181

7 156.0 INDU 0.001470 8.502181

8 155.0 INDU 0.001430 8.502181

9 154.0 INDU 0.001380 11.676328

[INDU] as-of merged CumDiv for Term1: from 3780 -> 3780 rows.

[INDU] as-of merged CumDiv for Term2: from 3780 -> 3780 rows.

[INDU] Dropped 0 rows missing TTM or Futures_Price.

Barndorff-Nielsen filter: flagged 43 outliers in spread_INDU

[INDU] Setting 43 outliers to NaN for cal_INDU_rf & spread_INDU

[INDU] Final forward rates shape: (3780, 29)

[INDU] Sample final rows:

cal_INDU_rf ois_fwd_INDU spread_INDU

Date

2024-12-24 3.525951 4.287412 -76.146147

2024-12-26 3.485142 4.277498 -79.235563

2024-12-27 3.459165 4.277624 -81.845864

2024-12-30 3.446690 4.275913 -82.922307

2024-12-31 3.377212 4.274017 -89.680496

Combined spreads data (first rows):

| spread_SPX | spread_NDX | spread_INDU | |

|---|---|---|---|

| 2010-01-04 | 11.572066 | 22.661276 | 25.302054 |

| 2010-01-05 | 12.181110 | 18.151200 | 26.010192 |

| 2010-01-06 | 4.369103 | 24.426083 | 23.178006 |

| 2010-01-07 | 4.393865 | 14.026219 | 23.177080 |

| 2010-01-08 | 13.157910 | 8.811714 | 23.300181 |

Correlation matrix of spreads:

| spread_SPX | spread_NDX | spread_INDU | |

|---|---|---|---|

| spread_SPX | 1.000000 | 0.842434 | 0.894422 |

| spread_NDX | 0.842434 | 1.000000 | 0.745491 |

| spread_INDU | 0.894422 | 0.745491 | 1.000000 |

# 5. Exploring the Economic Significance of Forward Rate Spreads

def explore_economic_significance():

"""

Analyze the economic significance of forward rate spreads

"""

print("=== Exploring Economic Significance of Forward Rate Spreads ===")

# Process data for SPX (as an example)

index_code = "SPX"

fut_file = Path(PROCESSED_DIR) / f"{index_code}_Calendar_spread.csv"

if not fut_file.exists():

print(f"Missing futures file for {index_code}. Cannot proceed with exploration.")

return None

# Run the forward rate calculation

df_res = process_index_forward_rates(index_code)

if df_res is None or df_res.empty:

print("No valid results. Ending exploration.")

return None

# Set the spread column

spread_col = f"spread_{index_code}"

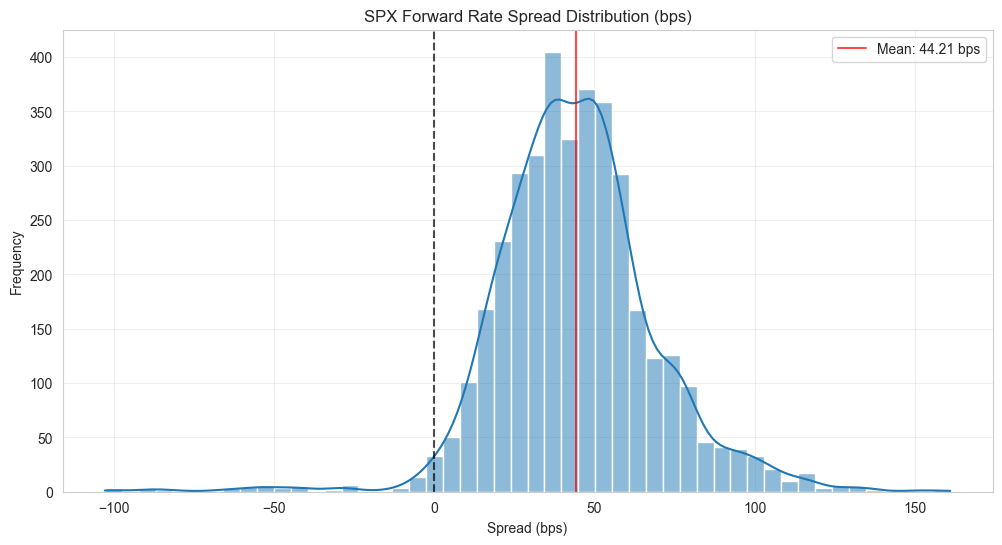

# Calculate the percentage of time the spread is positive vs negative

positive_spread = (df_res[spread_col] > 0).mean() * 100

negative_spread = (df_res[spread_col] < 0).mean() * 100

print(f"\nSpread direction summary:")

print(f" Positive spread: {positive_spread:.1f}% of the time")

print(f" Negative spread: {negative_spread:.1f}% of the time")

print(f" Zero or missing: {100 - positive_spread - negative_spread:.1f}% of the time")

# Visualize the distribution of spreads

plt.figure(figsize=(12, 6))

sns.histplot(df_res[spread_col].dropna(), bins=50, kde=True)

plt.axvline(0, color='k', linestyle='--', alpha=0.7)

plt.axvline(df_res[spread_col].mean(), color='r', linestyle='-', alpha=0.7,

label=f'Mean: {df_res[spread_col].mean():.2f} bps')

plt.title(f"{index_code} Forward Rate Spread Distribution (bps)")

plt.xlabel("Spread (bps)")

plt.ylabel("Frequency")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

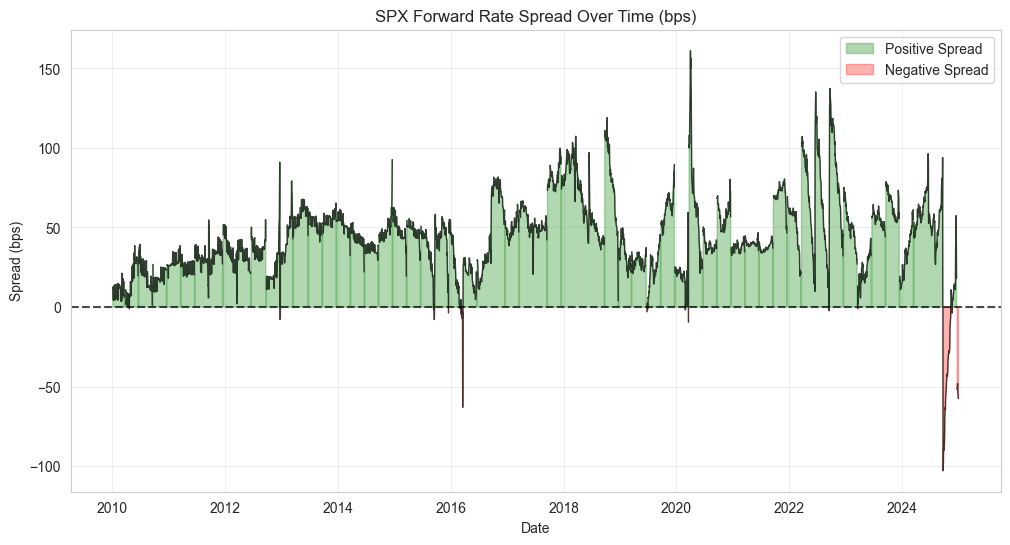

# Create a time plot with positive/negative highlighting

plt.figure(figsize=(12, 6))

# Plot the spread

plt.plot(df_res.index, df_res[spread_col], 'k-', alpha=0.7, linewidth=1)

# Highlight positive and negative regions

positive_mask = df_res[spread_col] > 0

negative_mask = df_res[spread_col] < 0

plt.fill_between(df_res.index, 0, df_res[spread_col], where=positive_mask,

color='green', alpha=0.3, label='Positive Spread')

plt.fill_between(df_res.index, 0, df_res[spread_col], where=negative_mask,

color='red', alpha=0.3, label='Negative Spread')

plt.axhline(0, color='k', linestyle='--', alpha=0.7)

plt.title(f"{index_code} Forward Rate Spread Over Time (bps)")

plt.xlabel("Date")

plt.ylabel("Spread (bps)")

plt.legend()

plt.grid(True, alpha=0.3)

plt.show()

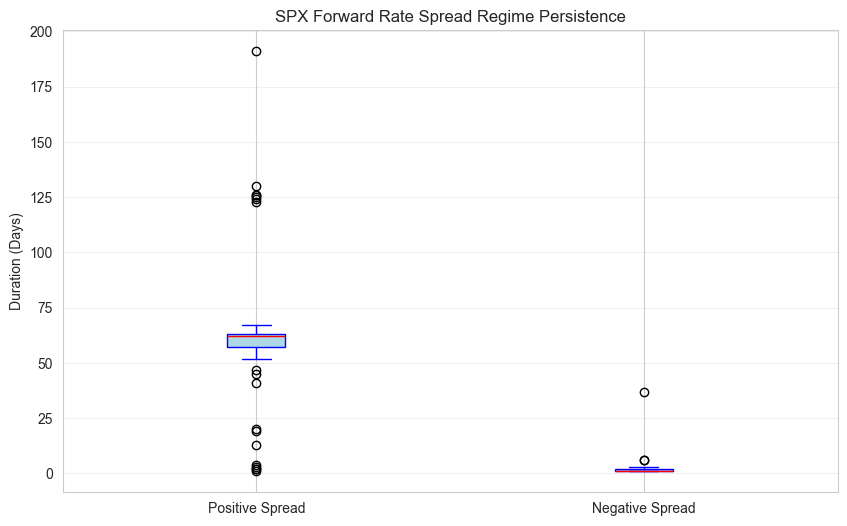

# Calculate persistence - how long spreads stay positive or negative

df_res['spread_sign'] = np.sign(df_res[spread_col])

df_res['regime_change'] = df_res['spread_sign'].diff().ne(0).astype(int)

df_res['regime_id'] = df_res['regime_change'].cumsum()

# Get regime lengths

regime_lengths = df_res.groupby('regime_id').size()

# Separate positive and negative regimes

regime_signs = df_res.groupby('regime_id')['spread_sign'].first()

positive_lengths = regime_lengths[regime_signs > 0]

negative_lengths = regime_lengths[regime_signs < 0]

print("\nRegime persistence:")

if not positive_lengths.empty:

print(f" Positive spread regimes: {len(positive_lengths)}")

print(f" Average positive regime duration: {positive_lengths.mean():.1f} days")

print(f" Longest positive regime: {positive_lengths.max()} days")

if not negative_lengths.empty:

print(f" Negative spread regimes: {len(negative_lengths)}")

print(f" Average negative regime duration: {negative_lengths.mean():.1f} days")

print(f" Longest negative regime: {negative_lengths.max()} days")

# Visualize regime persistence with a boxplot

plt.figure(figsize=(10, 6))

data = [positive_lengths, negative_lengths]

labels = ['Positive Spread', 'Negative Spread']

plt.boxplot(data, labels=labels, patch_artist=True,

boxprops=dict(facecolor='lightblue', color='blue'),

whiskerprops=dict(color='blue'),

capprops=dict(color='blue'),

medianprops=dict(color='red'))

plt.title(f"{index_code} Forward Rate Spread Regime Persistence")

plt.ylabel("Duration (Days)")

plt.grid(True, alpha=0.3, axis='y')

plt.show()

return df_res

# Run the exploration

economic_df = explore_economic_significance()

=== Exploring Economic Significance of Forward Rate Spreads ===

[SPX] Starting forward rate computation

[SPX] Loaded futures shape: (3781, 14)

[SPX] Dropped 0 rows lacking a valid Date in futures.

[SPX] as-of merged OIS: from 3781 -> 3781 rows (should be same).

[SPX] Building daily dividend table

Primary input file not found, switching to cached data

[SPX] daily dividends final shape: (3913, 2)

[SPX] Sample daily dividends:

Date Daily_Div

0 2010-01-01 0.000000

1 2010-01-04 0.058362

2 2010-01-05 0.001744

3 2010-01-06 0.497980

4 2010-01-07 0.061819

5 2010-01-08 0.000000

6 2010-01-11 0.000000

7 2010-01-12 0.000000

8 2010-01-13 0.113508

9 2010-01-14 0.021957

[SPX] as-of merged CumDiv at current date: from 3781 -> 3781 rows.

[SPX] Sample merged rows with cumulative div:

Date Term1_Futures_Price Term1_Volume Term1_OpenInterest \

0 2010-01-04 1128.75 1282633.0 2440458.0

1 2010-01-05 1132.25 1368386.0 2402850.0

2 2010-01-06 1133.00 1252015.0 2396493.0

3 2010-01-07 1137.50 1553963.0 2406352.0

4 2010-01-08 1141.50 1508175.0 2758348.0

5 2010-01-11 1142.50 1444997.0 2427453.0

6 2010-01-12 1134.00 2089364.0 2439036.0

7 2010-01-13 1141.50 2110033.0 2475322.0

8 2010-01-14 1145.25 1346436.0 2473392.0

9 2010-01-15 1132.25 2031715.0 2454453.0

Term1_ContractSpec Term1_SettlementDate Term1_TTM Term2_Futures_Price \

0 MAR 10 2010-03-19 74.0 1124.00

1 MAR 10 2010-03-19 73.0 1127.50

2 MAR 10 2010-03-19 72.0 1128.00

3 MAR 10 2010-03-19 71.0 1132.50

4 MAR 10 2010-03-19 70.0 1136.75

5 MAR 10 2010-03-19 67.0 1137.50

6 MAR 10 2010-03-19 66.0 1129.00

7 MAR 10 2010-03-19 65.0 1136.75

8 MAR 10 2010-03-19 64.0 1140.25

9 MAR 10 2010-03-19 63.0 1127.50

Term2_Volume Term2_OpenInterest Term2_ContractSpec Term2_SettlementDate \

0 1641.0 3354.0 JUN 10 2010-06-18

1 686.0 3432.0 JUN 10 2010-06-18

2 1163.0 3713.0 JUN 10 2010-06-18

3 1135.0 4154.0 JUN 10 2010-06-18

4 1080.0 17466.0 JUN 10 2010-06-18

5 419.0 4638.0 JUN 10 2010-06-18

6 481.0 4765.0 JUN 10 2010-06-18

7 1174.0 5389.0 JUN 10 2010-06-18

8 333.0 5357.0 JUN 10 2010-06-18

9 1432.0 5936.0 JUN 10 2010-06-18

Term2_TTM Index OIS CumDiv_current

0 165.0 SPX 0.001620 0.058362

1 164.0 SPX 0.001550 0.060106

2 163.0 SPX 0.001460 0.558086

3 162.0 SPX 0.001450 0.619905

4 161.0 SPX 0.001430 0.619905

5 158.0 SPX 0.001430 0.619905

6 157.0 SPX 0.001415 0.619905

7 156.0 SPX 0.001470 0.733413

8 155.0 SPX 0.001430 0.755370

9 154.0 SPX 0.001380 0.799620

[SPX] as-of merged CumDiv for Term1: from 3781 -> 3781 rows.

[SPX] as-of merged CumDiv for Term2: from 3781 -> 3781 rows.

[SPX] Dropped 0 rows missing TTM or Futures_Price.